Out of fear they’d become the next Greece, Western nations thought they must cut government spending. It now appears their actions increase the likelihood they are becoming the next Japan.

The shock of Brexit appears to be the catalyst for the recent capitulation, although we believe the reasons for sustained low interest rates are more structural.

Monetary economics is failing

In our February Investment Perspectives, we highlighted several reasons why low interest rates and Quantitative Easing will not work in addressing economic stagnation, namely:

- low interest rates generally work by encouraging private sector credit creation. Unless the private sector is willing to borrow, low rates will not stimulate growth. With private debt at or near record highs worldwide, sustained growth in credit is unlikely;

- as the Government is a net payer of interest, the non-government sector naturally is a net receiver of interest income. Low interest rates reduce net income to the private sector – effectively acting as an additional tax on savings; and

- quantitative easing involves the Central Bank acquiring high quality high-yielding financial securities for low-yielding cash. Again, this diverts net interest income from the private sector to the Government.

Central banks don’t yet see their actions (low interest rates) as deflationary. Unless there is a complete change in mind-set (like acknowledging that sovereign credit ratings do not matter), low rates are here to stay. In other words, insofar as lower interest rates stoke inflation, let the beatings continue until morale improves!

Investment implications

As a global listed real estate manager, one would think ‘lower for longer’ is positive for the asset class. Furthermore, low interest rates should be good for other yield-based investments as investors hunt for income.

However, low interest rates are not always good for real estate – much in the same way rising interest rates are not always bad.

The main problem with permanently low interest rates are the distortions it can create in the real economy over time. These distortions can take many years to ‘play out’ – but are worth considering today for long-term investors. The areas of distortion include:

- structural declines in company return on capital, feeding back to lower shareholder returns;

- falling net interest margin in the Banking sector; and

- potential to accelerate a supply response in real estate.

We discuss these distortions in greater detail below.

Low interest rates alter real investment decision making process

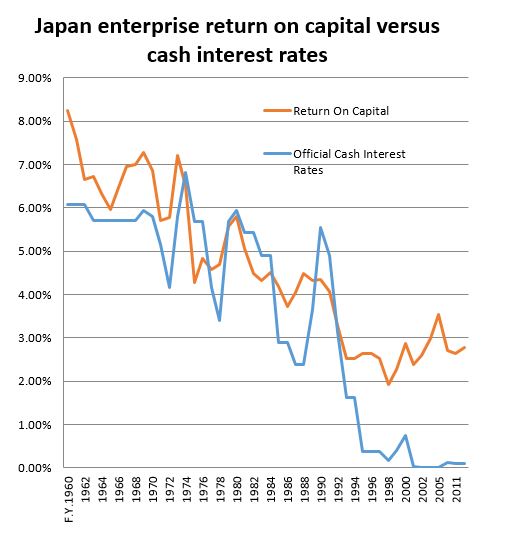

The poster child for sustained low interest rates is Japan. The Japanese economy is in no way disastrous. Unemployment has been quite low and real GDP growth per worker is actually better than most western economies post GFC (Japan +12% versus Europe flat). Yet inflation has remained stubbornly low. Much of this, we believe, is due to a structural decline in Japanese return on capital, which was driven by low ‘hurdle rates’. The ever-lower return per unit of capital has created an extremely low inflationary environment.

Source: Japanese Statistical Year Book, 6-12 & 6-13, Quay Global Investors

The lesson: as investors chase yield, they may make the mistake of assuming profits are sustainable. Yet in a low interest rate environment, the acceptance of lower returns on capital will feed itself back to shareholder returns, which is bad for stock prices. As we write today, the Nikkei 225 is around 57% below its 1989 peak after almost 20 years of zero interest rate policy.

Distortions in Banks

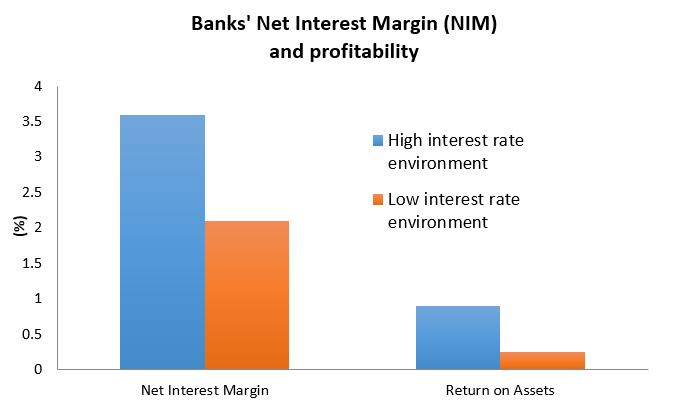

In Australia, one of the more favoured investment choices in a falling interest rate environment has been the Banks. Industry concentration and strong pricing power has ensured healthy margins – irrespective of the headline interest rate. Very high return on equity supported high dividend yields and growth.

But as Australian interest rates head lower, the risk is bank margins will contract. The net interest margin (the difference between the average funding / deposit rate and lending rate) will be very hard to sustain. Banks will be unwilling to price deposits at zero or less. Add some additional competition for lending as private sector appetite for new loans diminish, and margins begin to shrink.

This is more than just theory. A paper for the US Federal reserve highlighted that Banks that reside in a ‘low interest rate environment’ (three month bond yield < 1.25%) earned progressively lower net interest margins as interest rates declined. The risk is that Australian investors chasing a high-yielding bank today may have a very poor earnings outlook in a near-zero interest rate environment. Include the risk of rising bad loans (see below) and the ‘Bank’ story is far from compelling.

Source: IFDP Notes, Board of Governors US Federal Reserve System

Distortion in real estate

The distortions caused by low interest rates in Real Estate are no less pronounced.

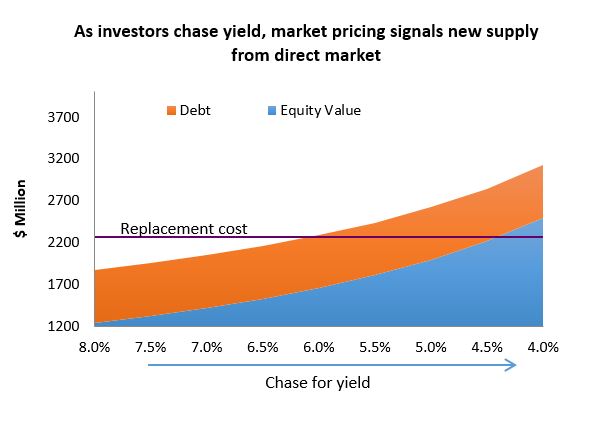

As investors chase yield in Real Estate, ever higher asset values (measured by implied and actual cap rates) bid up the underlying bricks and mortar. While short-term investors feel they are getting a better ‘yield deal’ compared to cash, what they may really be doing is acquiring the underlying property at a premium to replacement cost. This in turn encourages a supply response as the following chart demonstrates.

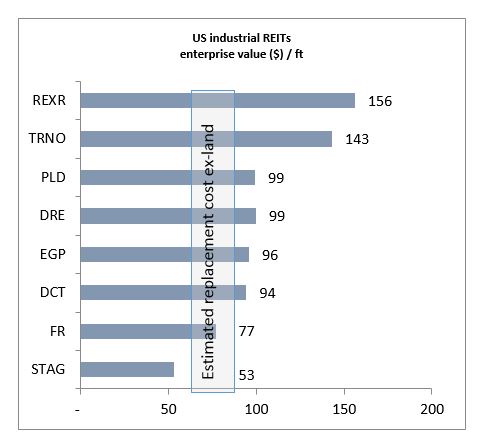

The risk to the Real Estate sector is more pronounced at the ‘commodity’ end of the real estate spectrum – such as Office, Industrial, and select Residential property.

The chart below highlights the issue for US Industrial REITs. They’re currently ’flavour of the month’ due to their e-commerce exposure, strong ’same store rent growth’ and yield, but investors have pushed enterprise values for many listed entities to a point that encourages new supply. Supply that is likely to be on-going until share prices reflect a discount to new stock.

Source: Bloomberg, Quay Global Investors

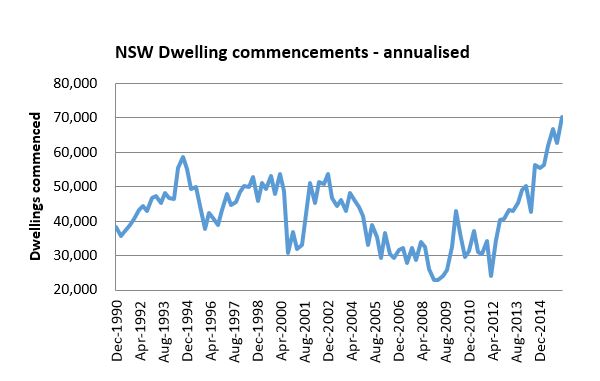

In Australia, since 2012 the RBA has progressively lowered the official cash rate (now 1.5%), which in turn has caused a significant increase in local property prices (especially residential). House and unit prices are now well above replacement cost resulting in a very significant supply response – especially in Sydney.

For investors who believe low interest rates will keep residential property prices elevated, we have to respectfully disagree.

We find the following chart a concern. Investors in Australian Banks should share this concern. Why? Because Banks effectively write Put Options against residential property, leading to leveraged exposure to a decline in property prices.

Source: ABS (Cat 8752.0, Building activity), Quay Global Investors

How does this fit with Quay’s investment strategy?

As a global listed real estate manager, we could be forgiven for cheering the 'lower for longer' interest rate environment. However, we believe sustained low interest rates and the ‘chase for yield’ will actually work against most investors over the long term. Not just in real estate – but across the economy, with particular concern for Financials and Banks.

Despite our concerns, we believe there are very attractive long-term global real estate opportunities in a low interest rate world. Real Estate that is hard to replicate (flagship malls, well located residential and retirement property as an example) will continue to do well. Even at the commodity end of the real estate spectrum there are assets still priced below replacement cost – albeit these opportunities are becoming rare.

Interest rates will be lower for longer. The key to investment success will not be allocating to yield – but by getting stock selection right.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.