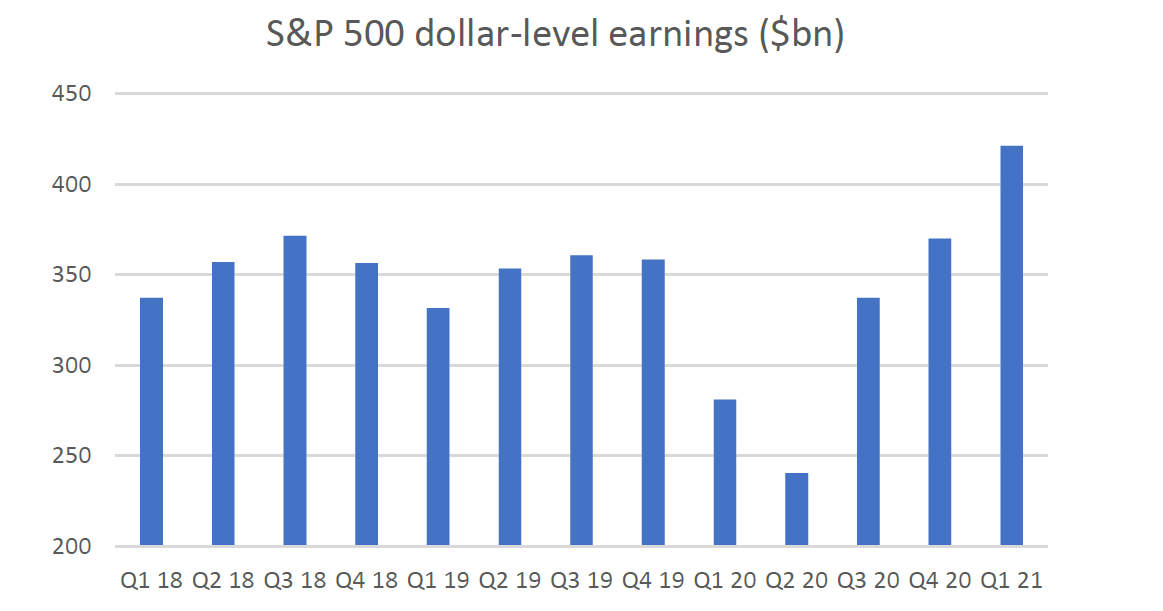

US corporate earnings (S&P 500) totalled US$421bn, up +27% compared to first quarter 2019 (pre-pandemic earnings). At a time when unemployment remains elevated, and supply disruption is causing production delays, these results may seem counterintuitive. So, what’s going on?

Source: Factset

Source of company profits

In 2019, we published an article titled Where do profits come from?, which drew on the Kalecki-Levy profits equation. The equation identifies the little-known relationship between company profits, government deficits, household savings, the current account deficit and national investment.

We encourage readers to read that article for a better understanding of this relationship. However, the equation itself can be summarised as:

Company profits = national investment + government deficits – household savings – current account deficit + dividends paid

The US data for this equation can be found at the Bureau of Economic Analysis website – our original paper provides the necessary links.

Since the onset of COVID-19, and the significant disruption associated with world economies, some investors and commentators have been caught short with the rapid recovery in share prices despite the significant uncertainty.

The profits equation, in our view, goes some way in explaining the robust first quarter earnings results and equity performance of world (especially US) sharemarket performance during the pandemic; and importantly, potentially points to a rosy medium-term profit outlook.

Checking in on Kalecki

Generally, the Kalecki-Levy profits equation is not always a great forecasting tool. It is better at breaking down the components and sources of historic corporate profits. However, by knowing the macro drivers, it’s possible to draw some rough forecasts based on prior household behaviour and current economic policy debate.

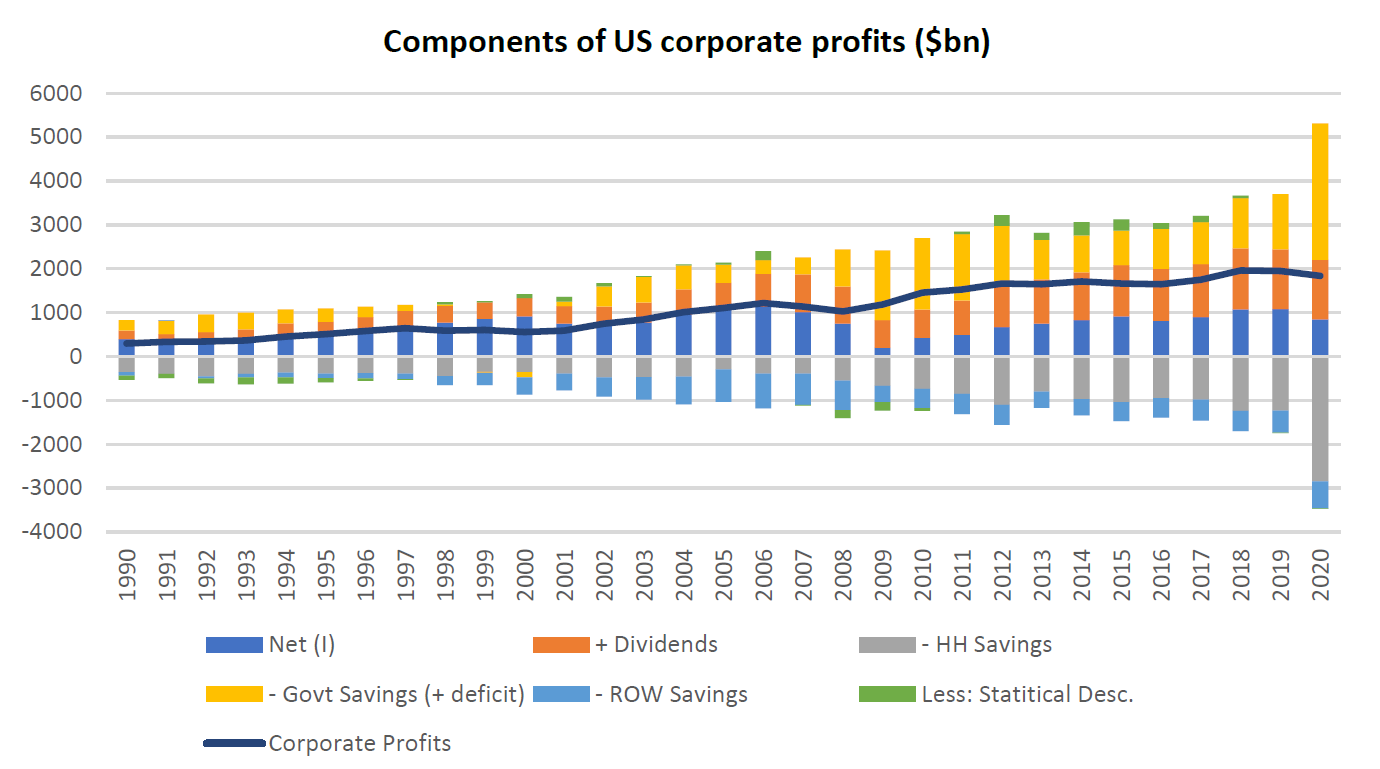

We last published the profit chart in 2019, using annual data to December 2018. Below is an update to December 2020 (which of course includes the pandemic).

Source: BEA, Quay Global Investors

The chart shows that company profits (including all listed and private companies), represented by the dark line, declined by just 6% to US$1,843bn compared to 2019 – a remarkable effort given the rolling shutdowns of many businesses over the year.

However, it is the components of the profits that are worth highlighting. The significant increase in net government spending (yellow) not only filled the coffers of households (grey), but also provided an offset to the decline in national investment (dark blue).

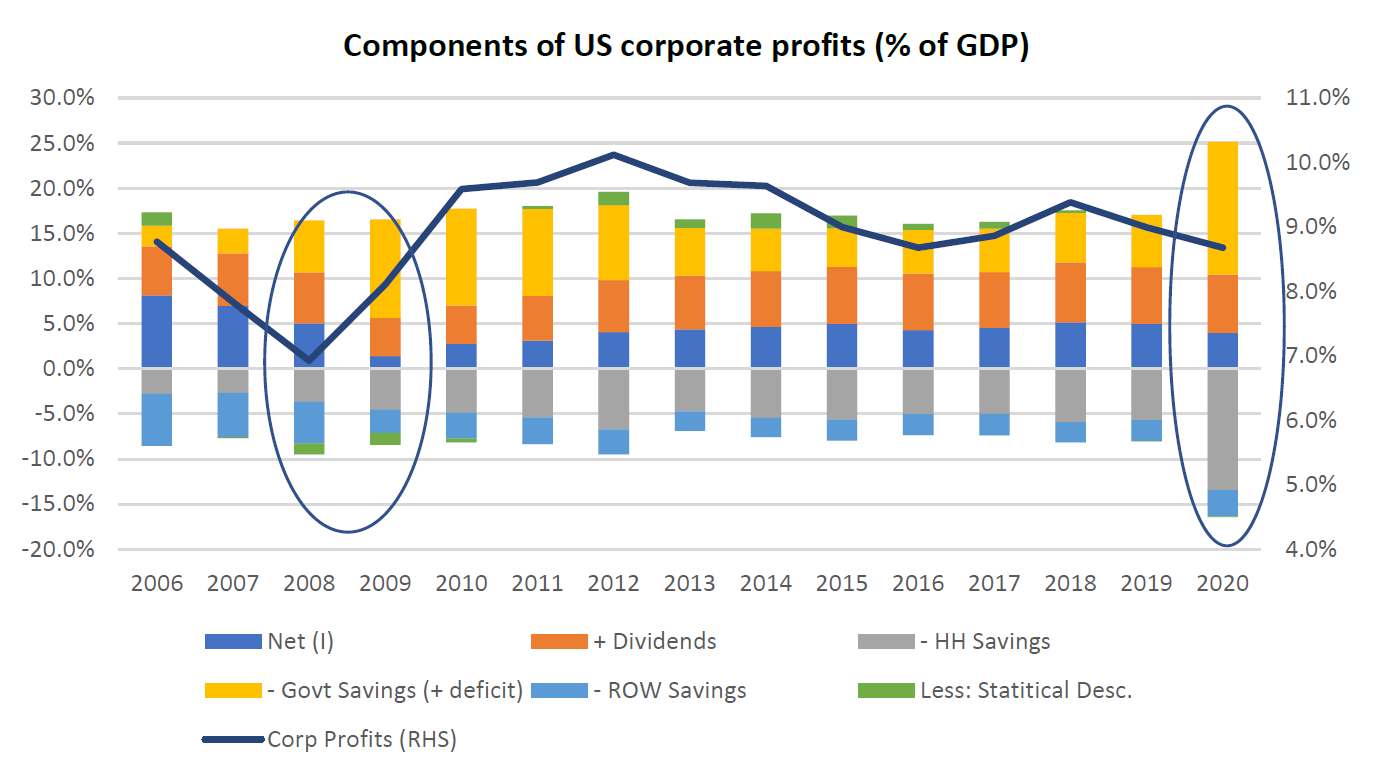

Taking a closer look at the data relative to GDP below, we can draw a number of interesting comparisons to the prior downturn in 2008-2009.

Source: BEA, Quay Global Investors

Some further observations include:

- The scale (relative to GDP) of net US government spending is meaningfully larger compared to the fiscal response to the financial crisis in 2008-2009

- The collapse in net investment in 2008-2009 was greater compared to 2020, and

- Household balance sheets have benefited significantly in 2020 compared to the 2008-2009 crisis.

What can Kalecki tell us about future profits?

As discussed, the profits equation is useful in identifying the historic macroeconomic components of company profits. In order to derive a forecast, one must attempt to accurately forecast each profit component – which, quite frankly, is very difficult to do.

But all is not lost! By knowing the components of company profits, we can identify policies and other trends to get a sense whether directionally, the profits outlook is rosy, or more uncertain.

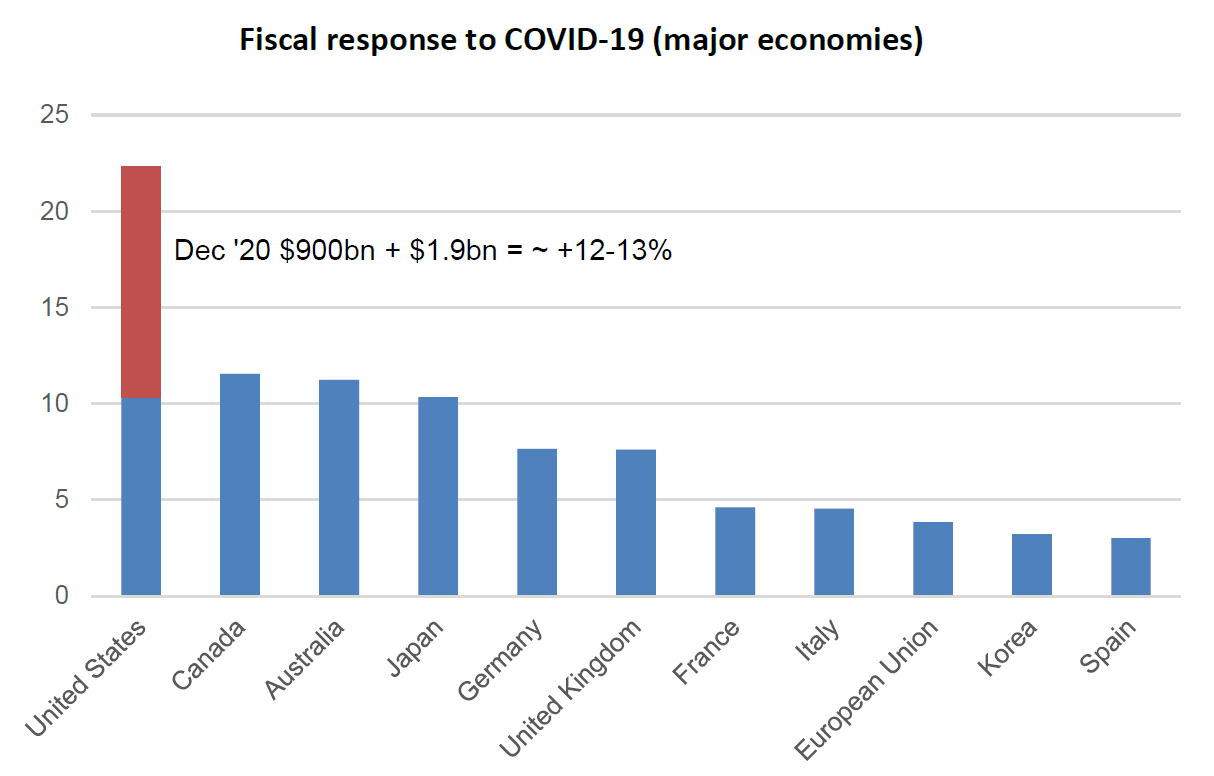

First, the above data is to December 2020. Since then, the US government has provided a further US$1.9T (9% of GDP) of additional COVID-19 financial relief. This takes the US fiscal response to COVID to ~22% of GDP (see below) and will add additional support to company profits going forward.

Source: IMF, Quay Global Investors

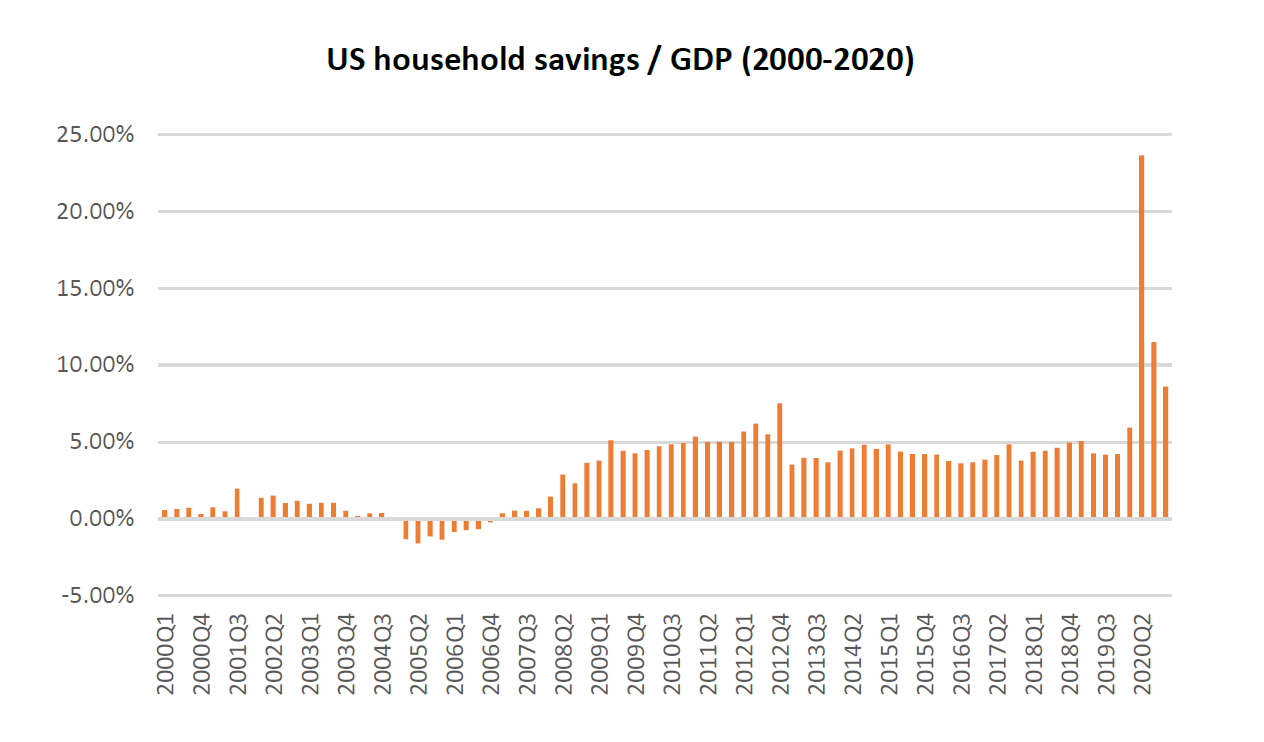

Second, as discovered earlier, the major beneficiary of the latest net government spending has overwhelmingly been households. This compares to the previous downturn where more than 50% of stimulus was in the form of tax cuts, bypassing most households. Isolating the household savings in the chart below puts this savings surge into context.

Source: St Louis Fred, BEA, Quay Global Investors

It seems unlikely US households will sit on this amount of cash indefinitely; rather, they will return to normal behaviour and run down their savings in line with history. All else being equal, this will add to future company profits as per the Kalecki equation.

Third, the weak US dollar post 2009 (fears of currency debasement via quantitative easing) reduced the trade deficit (foreign savings), adding to post 2009 earnings. We did not see this benefit in 2020, as the USD was unusually strong during the worst of the pandemic. It has since weakened (for similar fears of debasement), which should support corporate profits from a macro perspective.

Finally, the cornerstone to national savings and profits is net investment. And while this number did not decline as much as compared to 2008-2009, the prospects of what appears to be bi-partisan support for a US$2T (9% of GDP) infrastructure spend will meaningfully add to national investment, savings, and therefore corporate profits. In our view, the outcome of these deliberations will be more significant for medium-term sharemarket performance than anything the Federal reserve can or will do, and as such, is well worth monitoring.

How does this impact how we invest?

At Quay, we are unashamed bottom-up stock pickers. While we find this type of analysis interesting, it does not drive our investment process.

That said, our process and analysis has led the portfolio today to be comfortably overweight US real estate. Based on the macro impact of the Kalecki-Levi profit equation, and the fact the US fiscal response to COVID has dwarfed most other developed countries, there could be worse places to invest than the United States right now.

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.