Even in Japan, speculation has shifted to whether the Bank of Japan (BOJ) may dial back its easing program following the footsteps of the Federal Reserve and the ECB.

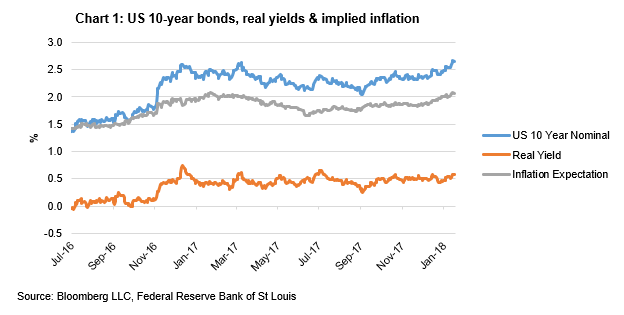

In response to this, long-dated government bond yields and inflation expectations have been rising around the world.

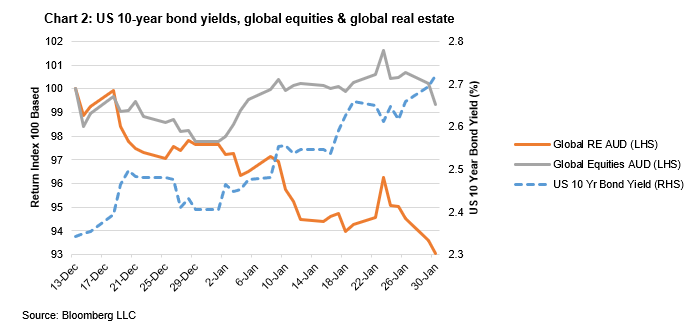

Rising long-dated interest rates and the ensuing enthusiasm for growth has predictably focused investors’ attention on those sectors that are regarded as ‘interest rate sensitive’. While US 10-year nominal bond yields have been on an upward trajectory for 18 months now, global real estate has underperformed global equities by ~6% since the middle of December last year (when bond yields spiked).

With such divergence in performance and uncertainty about where to for interest rates and inflation, an analysis of the historical impact of rising interest rates on the performance of global real estate is topical and timely.

We have previously provided analysis as to how real estate performs during a rate hike cycle. On this occasion, we have analysed the effect of the change in bond yields (outside of direct Fed policy).

The findings from this analysis support the observation that in the short-term, the pricing of global real estate is indeed adversely impacted – especially relative to other asset classes such as global equities. However, the adverse price movement in the short term usually leads to global real estate outperforming in subsequent periods in an absolute and relative sense.

Analysing periods of rising bond yields

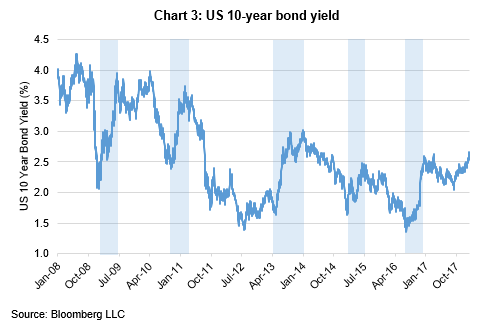

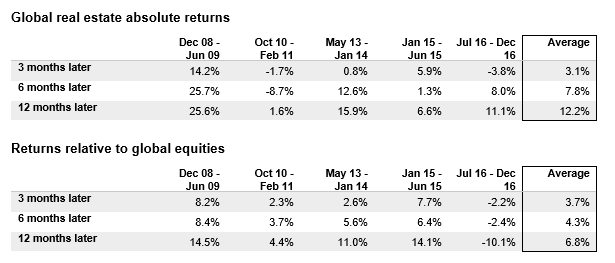

Over the past 10 years, there have been five periods of notable rises in the US 10-year bond yield (shaded blue in Chart 3). These periods were:

- Following the depths of the GFC in late 2008/early 2009;

- The announcement by the Fed of asecond round of quantitative easing (QE2) in October 2010;

- The ‘taper tantrum’ of 2013, coincidentally when the Fed said it would taper off its QE programs;

- The announcement by the ECB of its own QE program in January 2015; and

- The second half of 2016, when globally long-dated treasury yields started rising in response to central banks pulling back stimulus and as the market priced in a Trump victory.

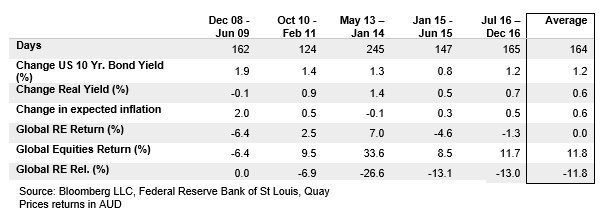

While the sample size is not large and the results far from conclusive, we can observe that in each of these periods global real estate did underperform global equities, with the exception being the period from December 2008 – June 2009 that spanned the lows of the GFC. This is highlighted in the following table.

With an average performance of -11.8% relative to global equities, the initial price reaction of global real estate to rising bond yields does appear adversely impacted, notwithstanding the share price return on average was unchanged.

However, rising inflation or the expectation of rising inflation is good for real estate returns. This is because rental growth is often tied to inflation, as are construction costs. Therefore, higher inflation means higher rent growth, but importantly supply is constrained by higher construction costs, thereby shifting the demand / supply equation in favour of the landlord.

Observing the returns for global real estate 3, 6 and 12 months after a rise in bond yields shows it has performed well in all subsequent time periods in both an absolute and relative sense.

Therefore, while prices react adversely or remain suppressed to the noise of rising interest rates and the expectation of rising inflation in the short term, when the noise settles down global real estate prices have a track record of recovering and outperforming global equities over subsequent timeframes.

How does global real estate perform in periods of rising inflation?

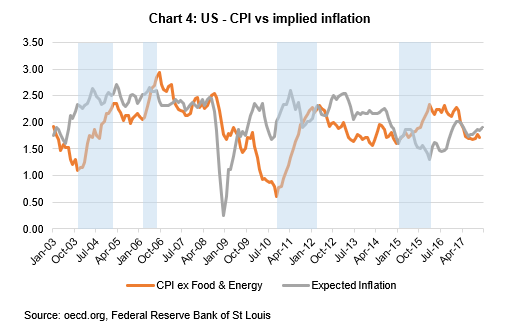

When bond yields are rising relative to real yields, implied inflation is also increasing. This, however, doesn’t always translate into actual inflation, as can be seen in Chart 4.

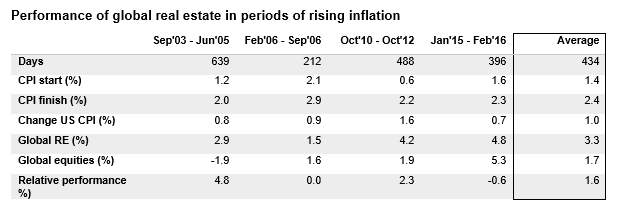

If, in the short term, share prices react to rising bonds and expected inflation, it would make sense that over the medium/longer term it will be actual inflation that in part influences returns. To better understand this, we have observed in the following table how global real estate has performed in periods of rising inflation (shaded blue in Chart 4).

The average return from global real estate is +3.3%, slightly ahead of global equities at +1.7%. What must also be remembered is that there are many factors at play over these periods that influence price, not just rising CPI.

Longer term relationship between bond yields, global real estate and other asset classes

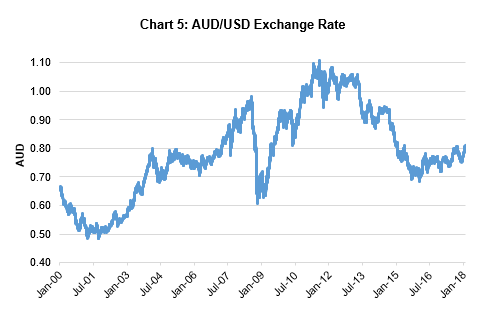

For a global unhedged investor, the exchange rate can have a significant impact on returns, particularly when making observations over shorter time periods. Analysing longer time periods provides greater perspective, and looks through the influence currency can have on the short term.

For instance, over the two years from 2006-08, the Australian dollar rose from US$0.70 to US$0.98. For an Australian investor in unhedged global real estate or global equities, this would have detracted 40% from total returns compared to a US investor.

However, since 2000 there has been a full currency cycle for the AUD against the USD, ranging from below $0.50 to above $1.10, and is now back to within 10 cents of its level in 2000.

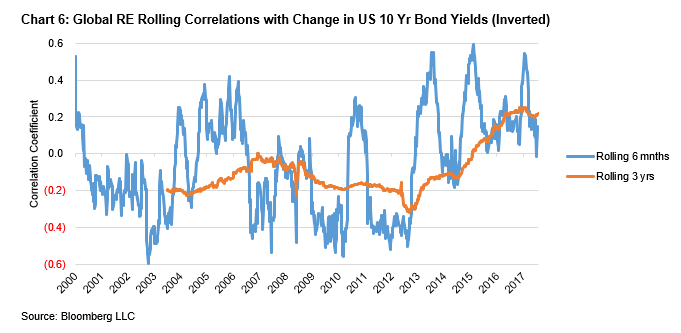

Over the same time the rolling correlation between the change in US 10-year bond yields (inverted) and global real estate has swung from positive (i.e. when yields rise, global real estate prices fall) to negative (when yields fall, global real estate rises). This can be seen in Chart 6.

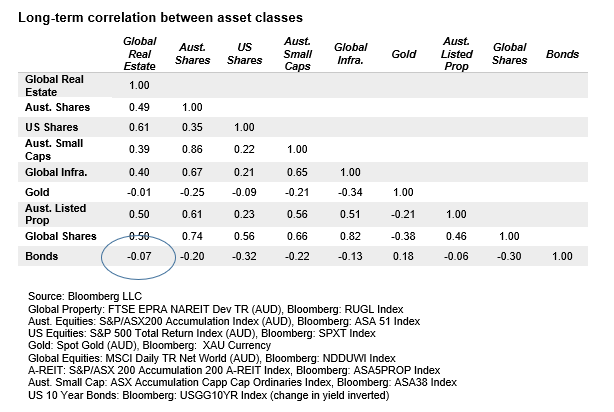

As the return horizon increases, the volatility in correlation smooths out – while over the long term, throughout a full currency cycle, there is almost no correlation to changes in US 10-year bond yields (-0.07 as per the following table).

Conclusion

Stepping back, what can we make of these observations? In the short term, global real estate prices are negatively impacted by rising bond yields and in almost all cases will underperform global equities. This is what we are witnessing now. However, when the noise settles, global real estate tends to perform well.

When inflation is rising, global real estate returns have in the recent past been modest and slightly better than global equities. However, these short-term observations are influenced by currency.

Over extended periods, the correlation to changing bond yields fluctuates, while over the longer term the correlation is almost non-existent.

It is worth noting that this analysis is also based on index returns. At Quay, we don’t invest in the index or manage our portfolio relative to any indices. We also don’t know when interest rates will stop rising, nor do we try and guess. The way we manage the portfolio is to focus on the fundamentals – making sure our investees represent the best possible global real estate opportunities we can find, in keeping with our process.

As long-term investors, the most relevant point is that over an extended period, the correlation between bonds and real estate pricing is zero. While there is plenty of noise around a ‘bondcano’ and the ‘end of the bond cycle’, over the long term we are confident our investments will deliver an acceptable return greater than inflation for our investors. Because in the long term, interest rates do not matter.