Why? Statistically, jail is the most visited square in the game and, after visiting jail, the orange squares are the most likely area that a player will visit based on the random outcome of two rolled dice, putting them in a ‘high traffic’ area – always a good proposition for property investment.

Furthermore, along with the green squares, the orange squares have the highest rent relative to price (i.e. return on capital).

Monopoly might be just a game, but identifying and buying the orange squares in real life – those with the best return on capital, and opportunities for high traffic (or demographic growth) – can help in real estate investing.

To us, the orange squares are:

- land rich with yield;

- driven by secular trends; and

- supported by demographics.

So where are the best ‘orange’ bets? Unlike Monopoly, where the opportunity to purchase depends on the roll of a dice, in property markets investors can be more strategic by identifying where future demand is likely to lie.

1. US housing

Yes, US housing. Many of the housing trends being unpicked in Australia are also present in the US. For instance, it is estimated that around 1.5 million young adults in the US still live with their parents. The ‘echo boom’ population – those aged between 20 and 34 – has the highest propensity to rent, with six out of ten renting.

And yet US housing supply remains in check, with little appetite to buy rather than rent. Purchase decisions are being delayed as people marry and form households later in life.

This makes for favourable rental growth conditions and presents interesting opportunities for investors.

Companies that supply apartment – ‘multi-family’ – homes with a focus on supply constrained markets along the west coast of the US, are well positioned to perform well.

2. Retiree accommodation

This encompasses a range of real estate options – not just aged care homes or healthcare and medical facilities, but also manufactured housing.

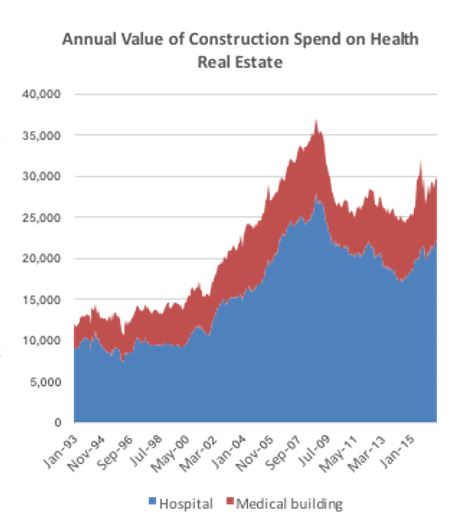

Aged and health care

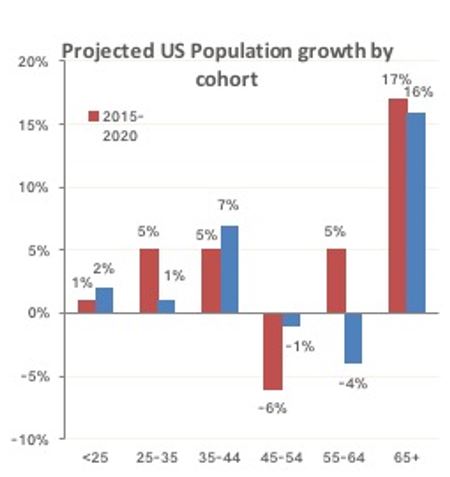

Longevity, demographic trends and healthcare policy is driving demand for care. The population groups made up of ageing baby boomers and those aged over 85 years are expected to grow at three times the rate of the overall population.

Meanwhile, approximately 10,000 Americans turn 65 every day, and will do so until 2030. Healthcare spending is projected to increase from 18 percent of GDP to 20 percent by 2022. And yet the industry displays all the traits of underinvestment.

Source: Bureau of Economic Analysis, Bureau of Labour Statistics

Source: Bureau of Economic Analysis

The opportunities for investment in this area are clear.

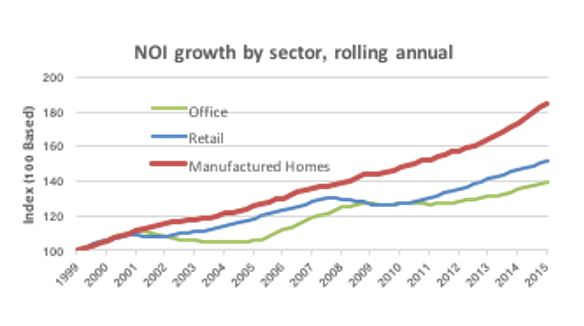

Manufactured housing

Manufactured housing describes homes built in factories that are then transferred to specific sites. Essentially, the home owner owns the house but not the site, where they instead pay a lease.

Such approaches are rising in popularity in the US, where they allow retirees in particular to live in areas such as Florida or California, which they may not otherwise have been able to afford.

The sites generate extremely predictable cashflow, and there has been strong income growth.

However, supply of manufactured housing in the US has been in decline since 1998, which is generating strong growth in net operating income (NOI) for suppliers, and for investors in these companies. History shows the underlying cashflows from this industry are virtually recession proof – and the industry’s best days are still ahead.

Source: Quay, NAREIT

3. Education

As higher education becomes critical for job opportunities, demand for student accommodation is increasing, particularly in markets such as the US and UK. In the UK, for instance, applications for places has outstripped acceptances since at least 2011, particularly in the wake of deregulation.

However, university stock levels are flat and private sector rentals are facing tougher regulation.

Companies providing purpose-built student accommodation can experience double digit earnings and medium-term earning growth through a combination of rental and external growth.

To Quay, these themes are the ‘orange squares’ – they are long-term, sustainable real estate investments that are generally less available in Australia.

Of course, knowing where not to invest can be equally as important. Some people might call these the ‘utilities’ or the ‘railways’ of the Monopoly game.

Sectors with potential long-term headwinds that may detract from future investment performance include the following.

Australian residential property

Australian residential property could perhaps be compared to the dark blue squares in Monopoly – expensive to buy, and offering uncompetitive returns.

There has been a notable surge in new supply in Australian dwellings over the past 18 months, with this forecast to continue for at least another 12 months. As a consequence, the return outlook from residential development in Australia is poor.

The current rate of new supply dwarfs anything we have ever seen in Australia for almost 40 years. While the population is growing, there's still a massive profit motive for developers to supply the market with new stock.?

Valuations in Australia, however, are clearly stretched and there is risk that some type of price correction is inevitable.

With so many other opportunities available to investors in property, it’s hard to make a case for exposing oneself to the current level of risk in Australian residential property.

Shopping centres

Retail property is a great example of where a truly active investment strategy can really benefit investors.

While high-end, ‘best-in-class’ shopping centres have the potential to thrive, there are a number of headwinds for ‘mid-market’ malls and the retail asset class in general.

As the mid-market is getting squeezed by a declining middle-class, retail landlords will need greater focus on the luxury retailers. The old retailer model of hundreds of stores will end, and retailers are likely to have significantly fewer stores to supplement their online offering.

Centres that do not fit this ‘best-in-class’ will have limited development opportunity and may become ‘capex machines’ – lots of capital for low return – in order to keep major tenants.

Investors should be wary of retail property as an investment, and choose their opportunities carefully, as there will be large variation in the performance of different assets.

Office property

Quay is becoming wary of the office property sector and recently sold its only pure office exposure.

A useful framework is to categorise certain types of real estate into ‘franchise’ or ‘commodity’. Commodity real estate is easily replicated; it therefore trades around replacement cost. We believe office property fits neatly into this category.

This framework helps explain the current office supply surge across key gateway markets around the world.

Low interest rates and the search for yield tends to push prices above long-term marginal cost, which in turn encourages a supply response.

In some instances, the supply response will deliver new stock right at the time demand potentially begins to weaken - for example, London following Brexit, where the vacancy rates are forecast to reach 11 percent by 2019 in the City, almost double where they are today.

Moreover, office property tends to have very high ongoing capital expenditure requirements due to high levels of tenant incentives and leasing commissions, and high build-to-land ratios, resulting in high economic depreciation rates (especially in urban locations).

As we enter the ‘supply response phase’ of the cycle, we think it is probable that the best of office property returns is now behind us.

Overall, while real estate investing is definitely not a game, there are some basic rules, and some helpful data, that can help investors come out ahead, as long as they take a strategic approach.