There continues to be some concern how financial markets will react if/when the US Federal Reserves begins a cash rate tightening cycle. The strong October employment report suggests this cycle may begin as early as December.

Many assume rising US interest rates will be a headwind for listed real estate performance. For investors who view listed real estate as a proxy for bonds or as a ‘yield play’, this view is understandable. However, real estate is not a proxy for bonds – nor should it be viewed as simply a yield instrument. It is a risk asset that generates a total return comprised of yield and growth. Therefore, it is in no way a certainty that rising US interest rates will be a negative for listed property.

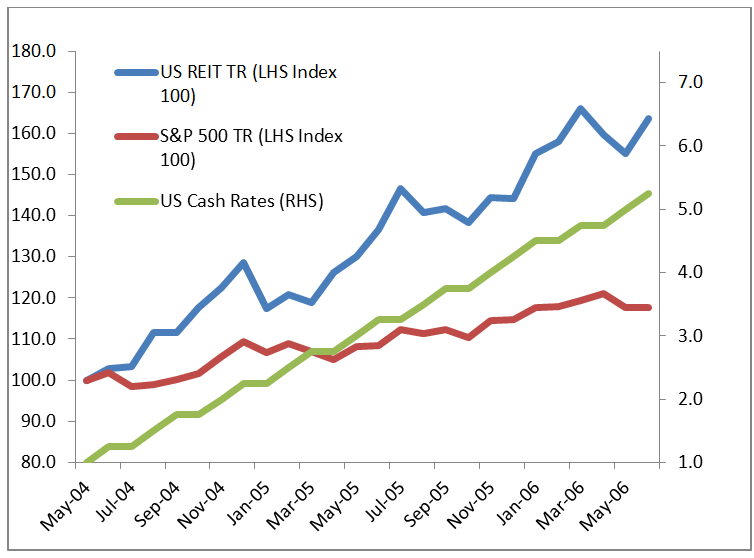

To understand this point better, it is interesting to look back to when the US Federal Reserve last initiated their tightening cycle (that is, the first increase in interest rates from the last cut). This happened in June 2004 when the upper bound cash target rate was increased 0.25% to 1.25%.

So how did listed real estate (US REITs) perform in the following years until the last rate hike?

Source: Bloomberg, Quay Global Investors

As the chart shows, US REITs performed strongly in an absolute sense (up 63.6%) and in a relative sense (outperformed S&P 500 by 38.9%) to the last tightening date June 2006.

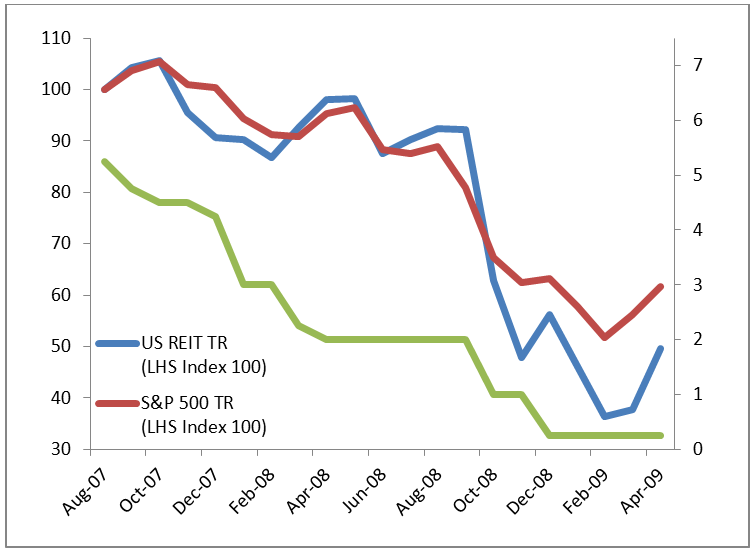

And when cash rates were cut from August 2007 through to December 2008, US REITs underperformed, further discrediting the assumed link.

Every cycle is different

Of course, many will point to the real estate bubble in the early 2000s as the source of strong relative and absolute performance. But the bubble was largely confined to the unlisted residential home market rather than commercial. Undoubtedly, each cycle is different. So what is different this time?

From a real estate perspective, the main difference is that supply remains (generally) well contained. Retail, Storage, Residential and Skilled Nursing Facilities all remain supply constrained for various reasons. Fundamentally, low supply augurs well for rental growth.

Of more concern is the outlook for equities. We believe there is a strong case that rising US interest rates could be significantly negative for equity investors – while real estate remains relatively well protected.

Has profit share peaked?

One of the strong tailwinds for US (and global) equity performance since 2009 has been the ongoing weakness in the labour markets while economic growth has remained positive. This had three consequences:

- top line growth for companies remained positive;

- per unit labour costs declined; and

- significant corporate margin expansion.

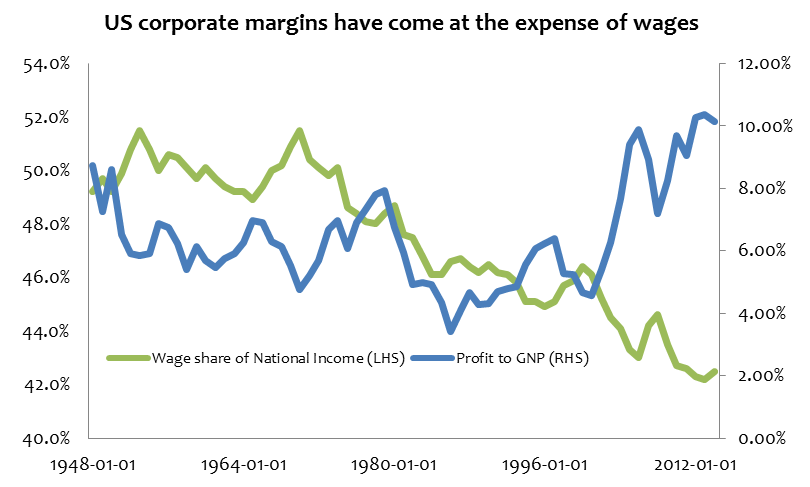

In essence, the past six years of economic activity has provided the perfect storm for owners of equity. The chart below shows US profit share has surged, largely coming at the expense of wage earners.

The important point to note is the US Federal Reserve will consider lifting interest rates because they believe the labour market had (or will continue to) recover. If true, over time we can expect wage share to stablise and even improve. Readers with a keen eye will notice in the chart above perhaps this trend has already begun. The consequences for equities are:

- slightly better sales as GDP growth accelerates;

- lower margins as wage claims increase; and

- higher discount rates as interest rates rise.

The downside is not insignificant. If profit share moves down from its current level of 10% to 8% (which is still high by historic standards) due to improving wage claims, this represents a 20% fall in profits relative to GNP. Assuming nominal GNP growth of, say, 5% p.a., then nominal profit growth (before any change in share count) could be flat for four years.

In short, the scenario is flat or falling free cashflow in the face of rising discount rates.

How is Quay’s portfolio positioned?

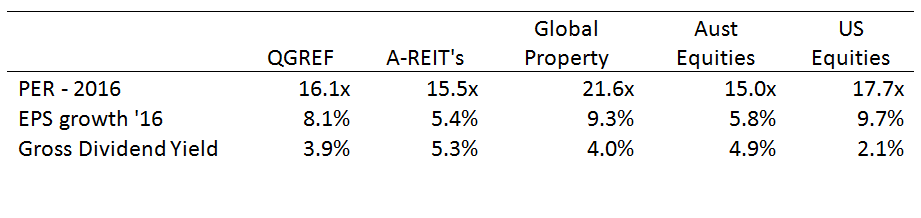

The Quay Global Real Estate Fund (the Fund) remains invested across 26 companies and five countries, and diversified across multiple asset classes. Based on current pricing, the Fund has average price earnings ratio lower than select peers and higher EPS/FFO growth which will assist in the face of higher discount rates.

We believe the portfolio’s combination of a relatively low PER and competitive FFO growth rate, along with the long-term demographic tailwinds that we believe are at our advantage, makes us well placed to meet our long-term investment objectives if or when interest rates begin to rise.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.