Dad, are you coming?

In a recent conversation my son raised two seemingly unrelated topics. First, whether his teacher was correct in that governments can’t simply spend forever, as people will just stop lending them money. He later reminded me that if I wanted to come to the school play, I needed to get tickets.

I used the opportunity to link the two topics. I began,

“So, to come to the play I need a ticket?”

“Yes, but don’t worry they are free.”

“Even though they are free, these tickets are valuable. I can’t get in without one?”

“Um, I guess.”

“So maybe it will be good for the school to issue only a few tickets, then on the night they can collect more, generating a surplus of tickets. This will be good for the school since we just agreed these tickets are valuable.”

“Don’t be dumb Dad.”

Yes, I agree, my last statement was dumb. But it is no less dumb than mounting an argument that the recent sell off in bonds is due to ‘too much debt’, and a general unwillingness for investors to buy US bonds.

Currency, just like the tickets for the school play, must be issued first before they can be collected. For a school play, the tickets are collected at the door. For the currency, the issued currency is collected via the issue of bonds or taxes.

Getting the order right is important. It is the government deficit (issuing of the currency) that funds the purchase of the bonds. Just as the issue of tickets is required before collecting them. In that context, there always enough money to buy the bonds.

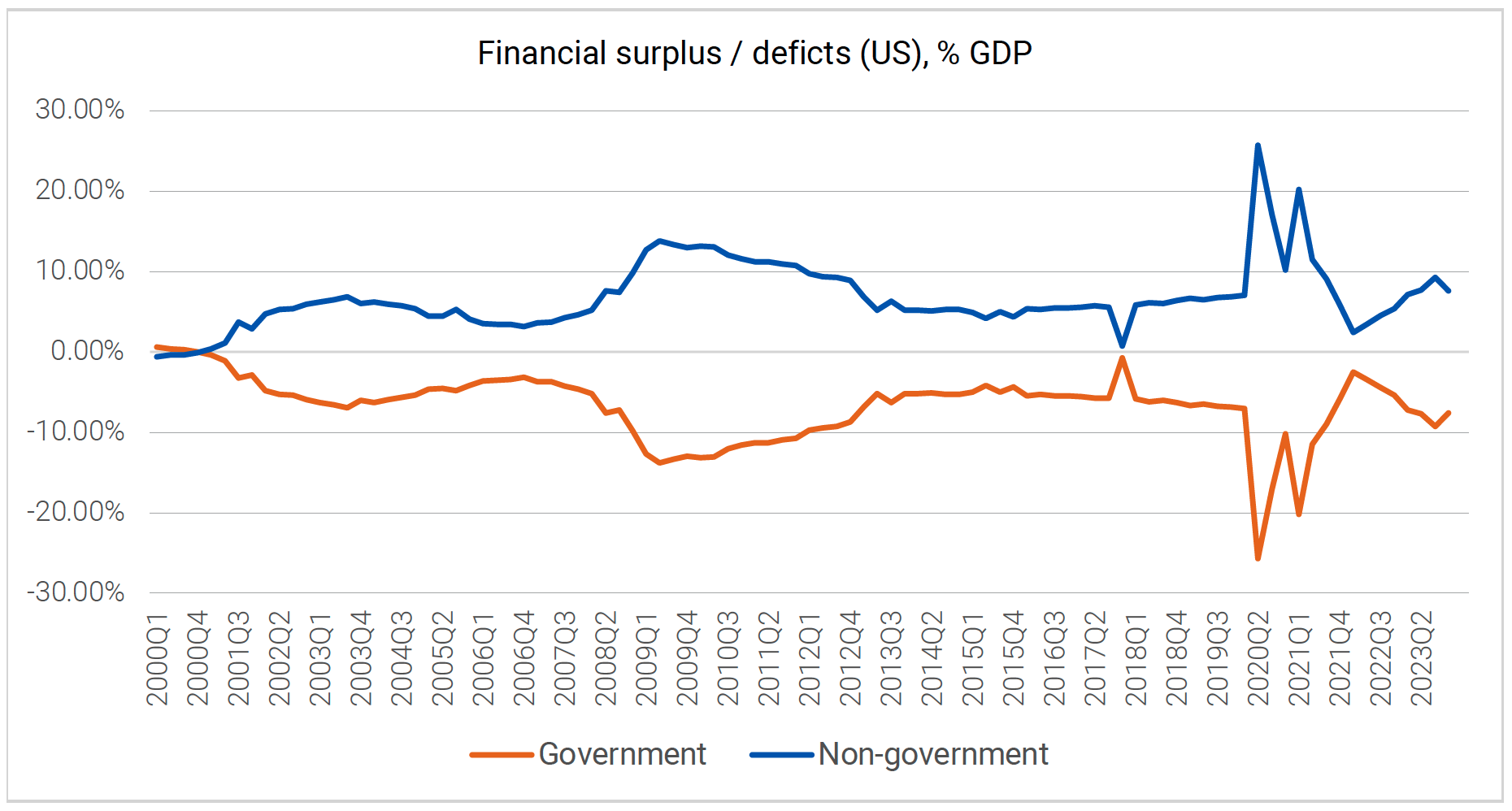

We see this more clearly when viewing a simple sectoral balances chart – split between the government sector and the non-government sector. It shows empirically the size of the government deficit is always matched by the size of the non-government savings pool savings. To the Dollar.

Source: US Federal Reserve, BEA, Quay Global Investors.

Source: US Federal Reserve, BEA, Quay Global Investors.

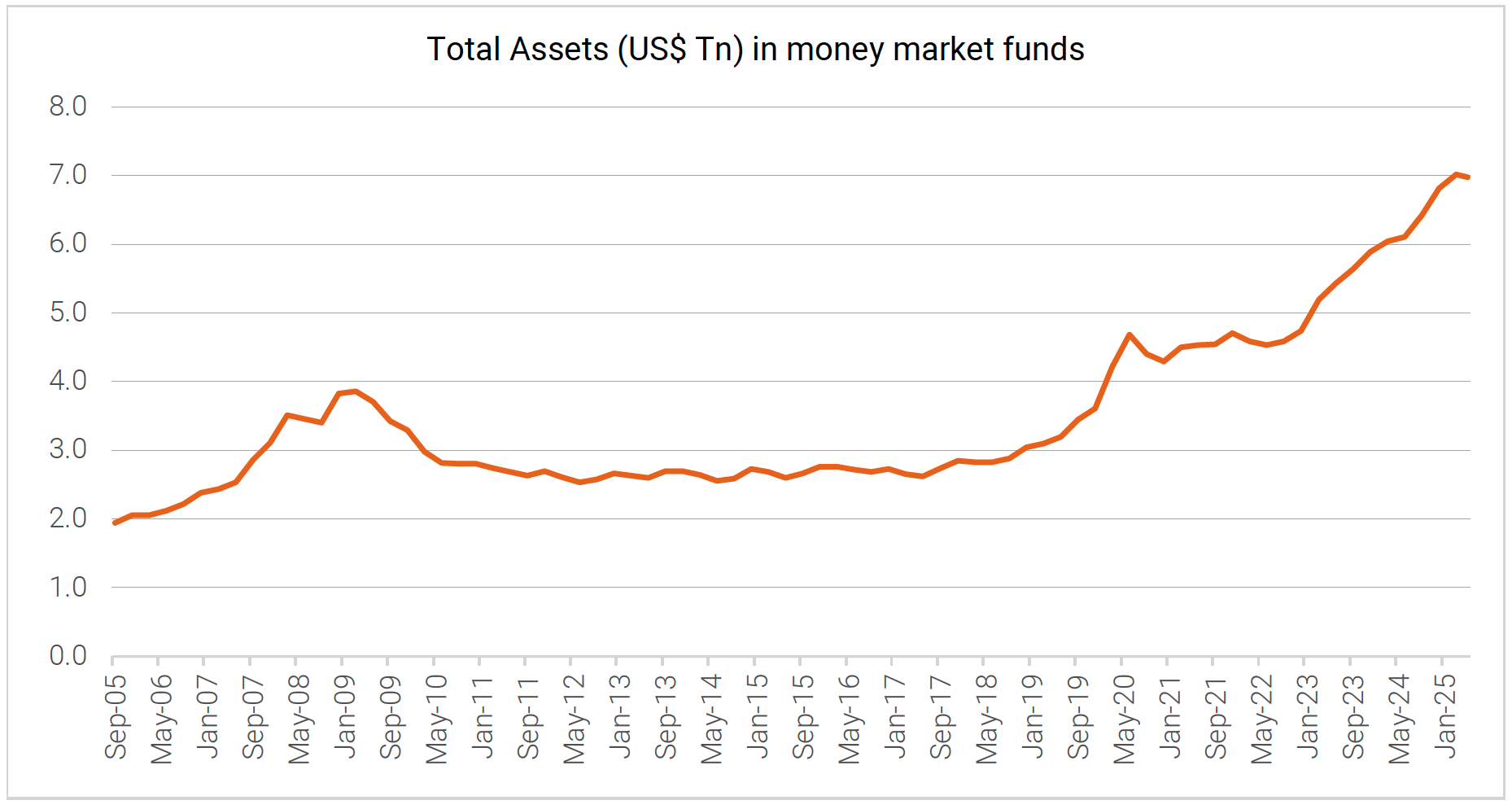

These savings accumulate in various ways, including simply showing up in higher cash balances in banking accounts. Another sign of these accumulated savings is in money market accounts, which (not surprisingly) have surged in line with the higher US Deficit of the 2020s.

Source: Bloomberg, Quay Global Investors.

Source: Bloomberg, Quay Global Investors.

What if not everyone shows up?

Taking the analogy further, just because the school issues (say) 200 tickets, does not mean all ticket holders will show up on the night. Could the same be said for the bond market?

We feel this has been the primary concern of markets over the past month or so. While investors have the financial savings to buy the bonds, it does not mean they will always show up to the auction. Especially now the debt (for the US) has been downgraded.

But for the bond market it doesn’t end there.

Net government spending ultimately shows up as cash in recipients’ accounts. The stock of cash created is constant – that is even if an individual wished to use their cash to buy an asset, the seller of that asset ends up with the cash. So, in a macro sense the total cash in the system is fixed.

Cash is nothing more than a zero duration, zero coupon bond, both issued by the treasury. By preferring cash over a bond, an investor is expecting a higher return over the duration period. Or said another way, the cumulative return on cash is expected to be higher than the IRR of the bond. So potential buyers hold back until the bond yield meets an indifference point, ie where (at a macro level) investors are indifferent between holding cash and bonds.

So, bond demand is not about volume (ie, is there enough money to buy the bonds), but about price (is there a better return on the bonds versus holding cash).

Why have bond yields been rising?

Since the bond market is not reliant on volume, bond yields have been rising to compensate for higher expected long term cash rates. In the US this is almost certainly caused by expectations of a ‘expansionary’ US budget deficit via the new ‘big, beautiful bill1’.

Is the current Administration budget policy expansionary? At the time of writing, there have been some scary headlines suggesting the new spending bill would add trillions to the budget deficit2. In an economy that has been running close to full capacity, the natural fear is a more expansionary deficit will be inflationary. That, in turn, means a more hawkish Fed policy stance, hence high bond yields.

While the full details of the latest US tax and budget bill have not been fully released, we put forward a few observations:

- Most of the bill centres around the extension of the 2017 Tax Cuts and Jobs Act (TCJA), which were time-limited when first passed.

- When calculating (or scoring) the budget impact from the extended tax cuts, it is assumed the 2017 tax cuts expire (raising forecast revenue) and are then re-established (reducing forecast revenue)3.

- The ‘adding to the deficit’ measures the debt from a baseline the 2017 tax cuts expire – so headlines stating the budget is “adding trillions” to the debt reflects what is happening if the tax cuts expired, which would have reduced the deficit by ‘trillions’.

- So, in other words, most of the tax bill is just a continuation of the current state of play.

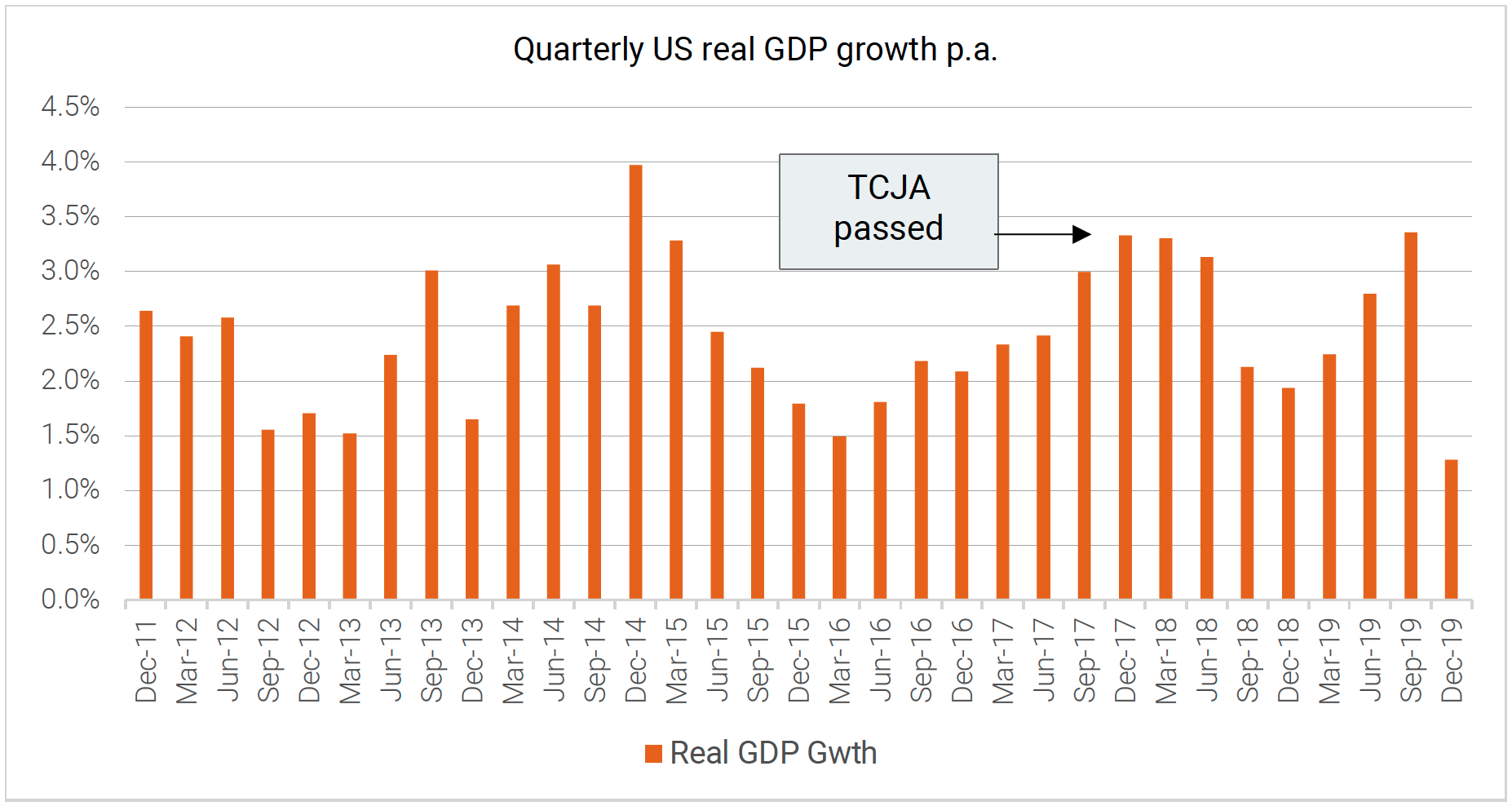

Of course, there are other measures in the bill that could be stimulatory, although by our observation they seem small. And as a reminder, regressive tax cuts rarely trickle down or add to economic growth. As the charts below highlight, the significant tax cuts that passed in December 2017 via TCJA barely impacted economic growth or jobs.

Source: BLS, Quay Global Investors, CBO.

Source: BLS, Quay Global Investors, CBO.

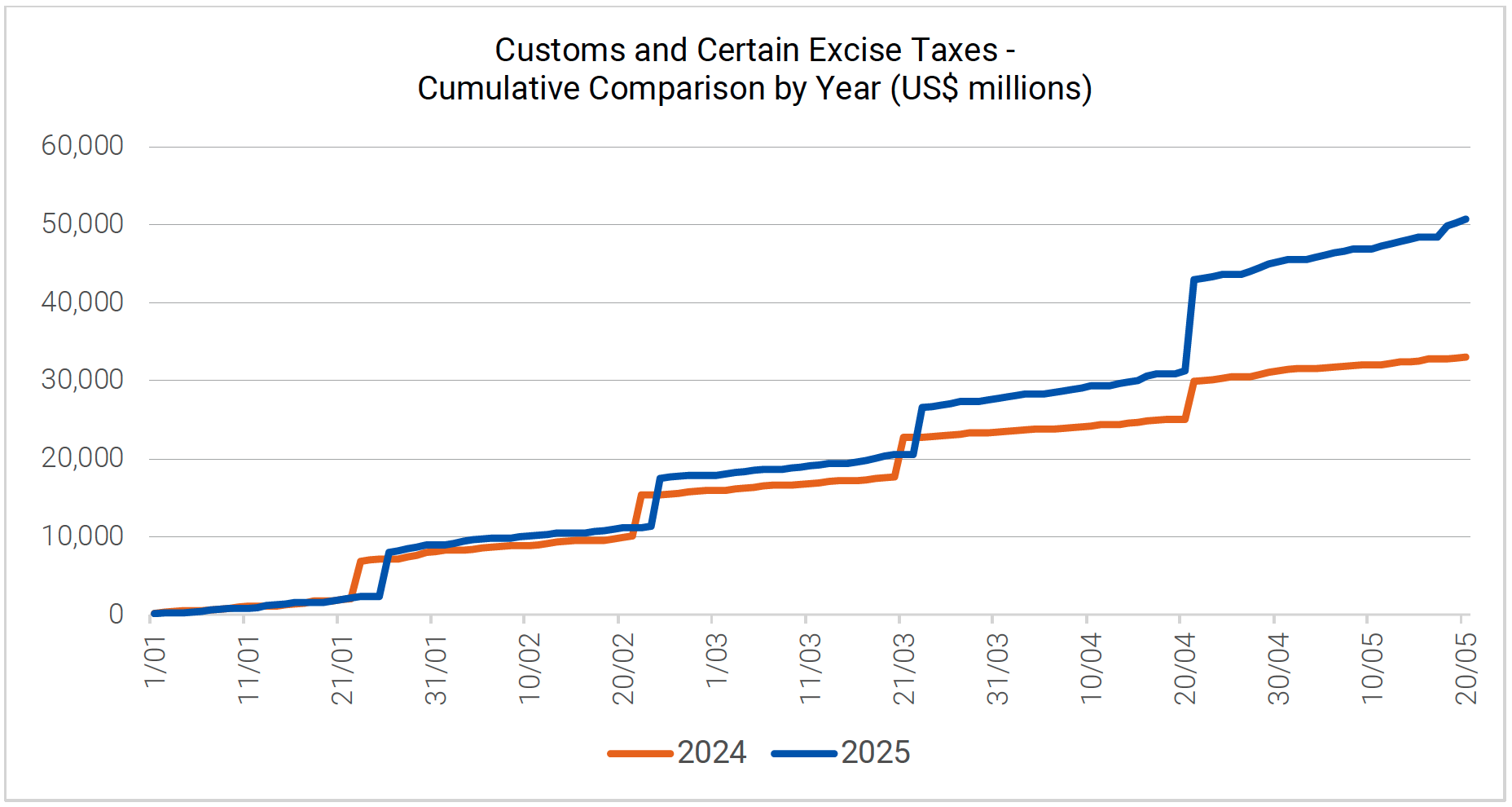

Meanwhile, the recently announced US tariffs are already having an impact on government finances (therefore non-government finances). Tariff collections are now running ahead of last year, draining the non-government sector of financial resources. The regressive nature of tariffs (essentially a flat sales tax) is a headwind for growth.

Source: US Treasury, Quay Global Investors.

Source: US Treasury, Quay Global Investors.

Impact on listed REITs

Listed REITs have again felt the impact of the short-term change in long term interest rates. We believe this will continue to dis-incentivise new supply which is already somewhat suppressed. Lack of incremental supply will inevitably lead to a demand and supply imbalance, handing negotiating power to existing landlords.

We see the impact of this demand-supply imbalance in two sectors today – Data centres and Senior housing, where double digit per annum net rent growth is not uncommon. These REITs have increased 50-100% over the past few years despite a rising bond yield environment. But we see this dynamic as a forerunner for other real estate sectors as incremental supply abates and landlord pricing power returns.

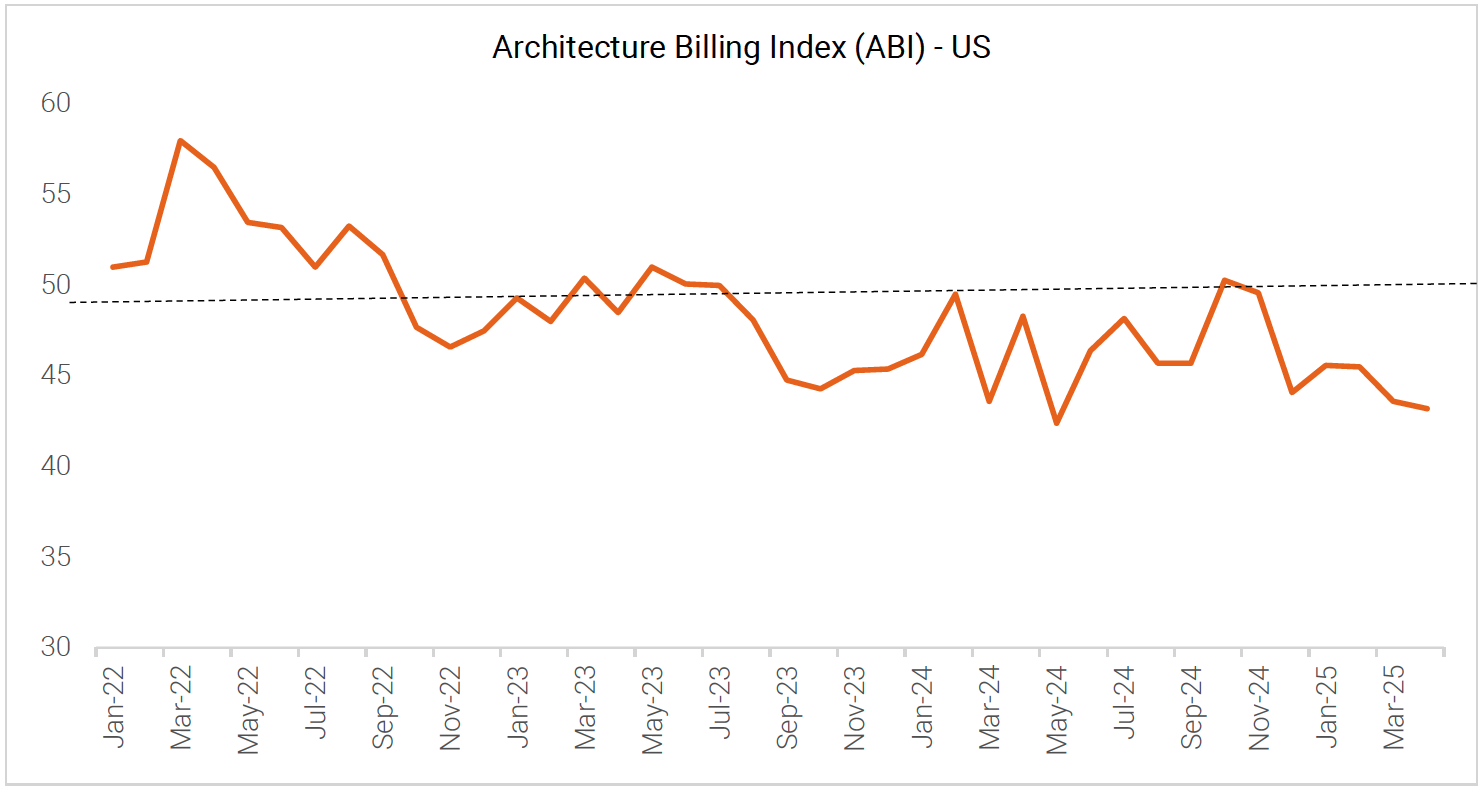

As we wrote last month, the AIA Architecture Billing Index (a lead indicator for commercial construction) continues to contract – now down 28 of the past 32 months. And although the US economy is not officially in recession, many architecture firms are reporting recession-like conditions4.

Source: AIA, Quay Global Investors.

Source: AIA, Quay Global Investors.

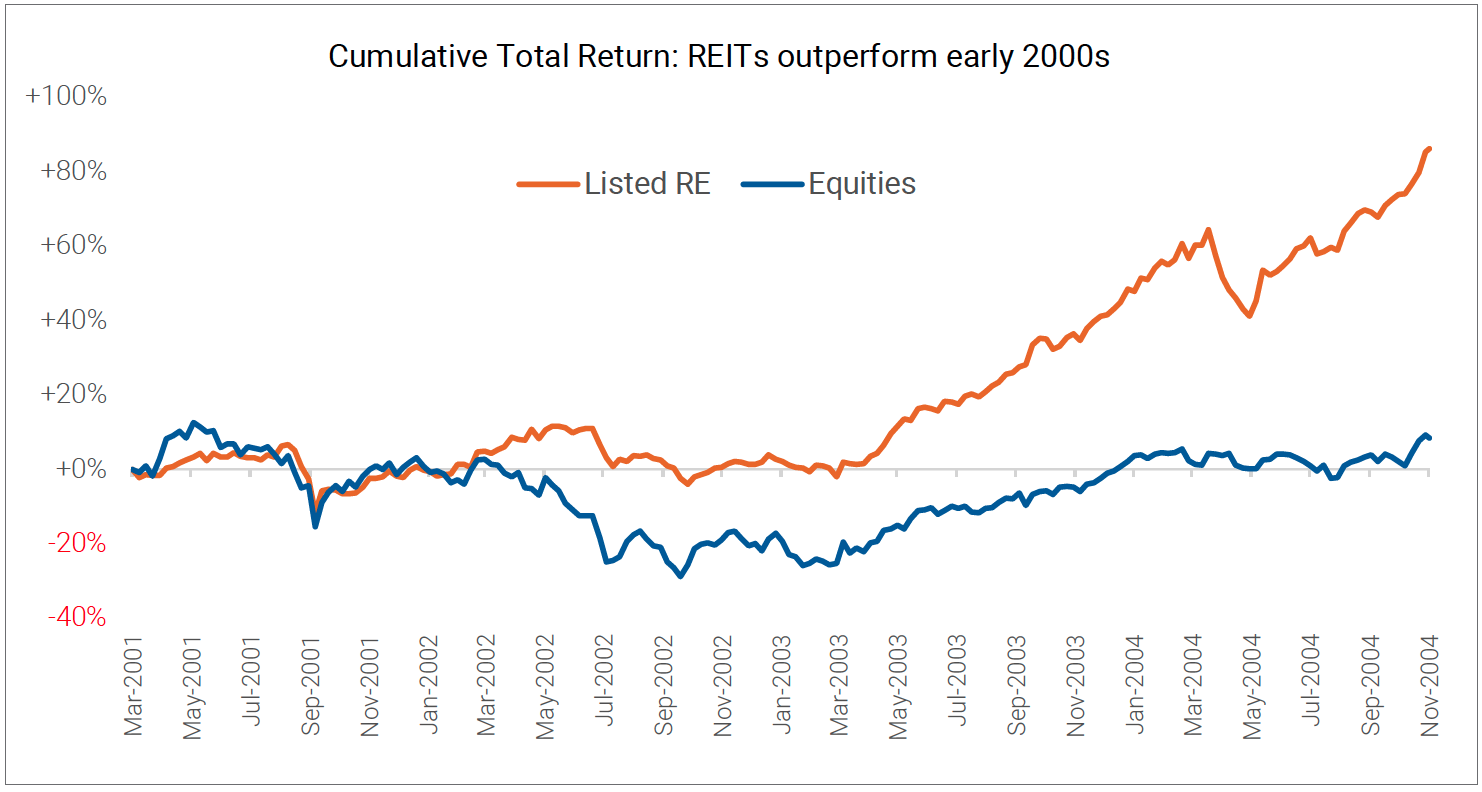

In the past, sustained undersupply led to strong long term outperformance for listed REITs, as seen below, during the early 2000s (while the US Federal Reserve was increasing interest rates).

Source: Bloomberg, Quay Global Investors.

Source: Bloomberg, Quay Global Investors.

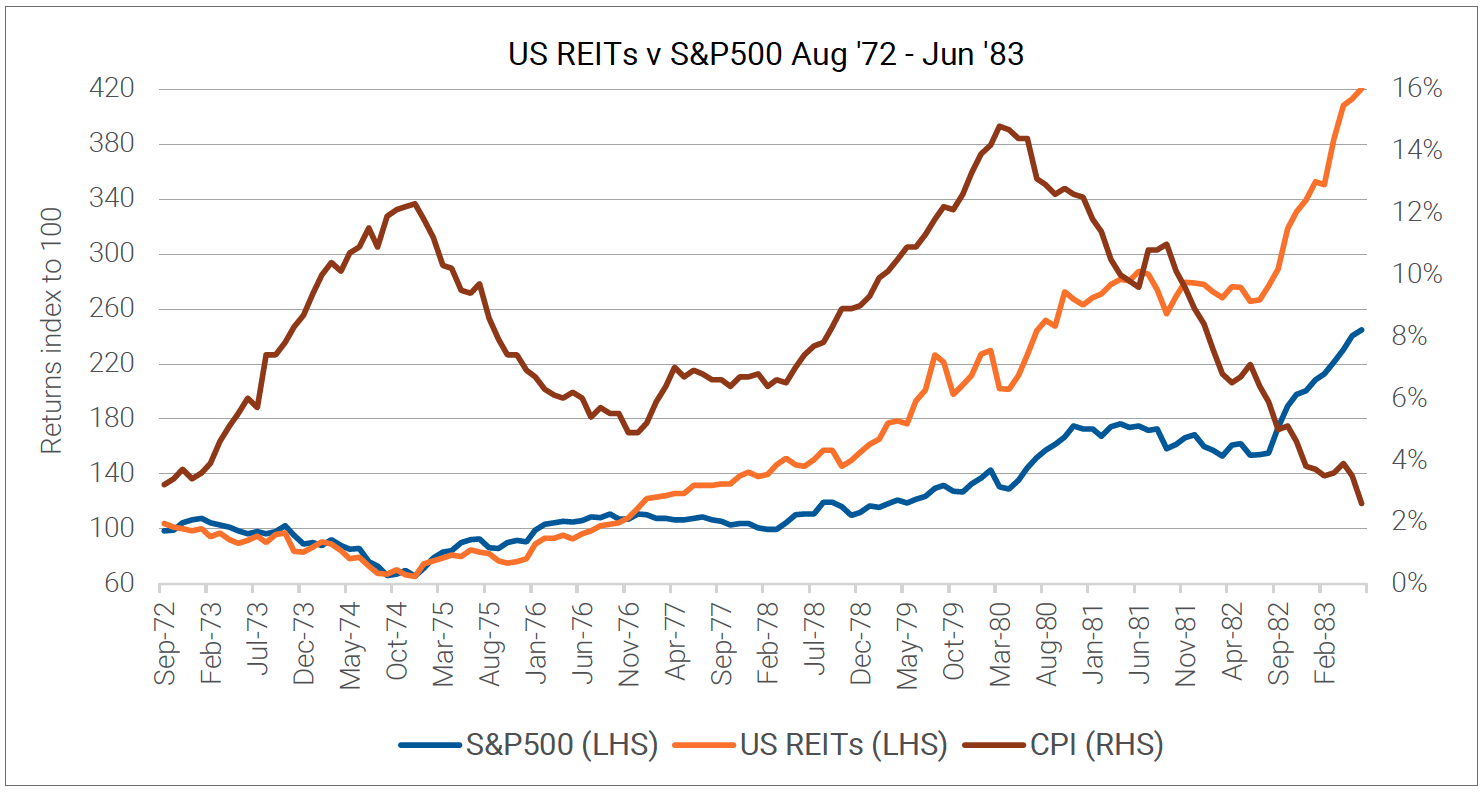

And again, in second half of the 1970s during the second inflation shock, building costs pushed above market values crimping supply and leading to outsized landlord pricing power (and REIT performance).

Source: NAREIT, Quay Global Investors.

Source: NAREIT, Quay Global Investors.

Concluding thoughts

It is important to frame recent bond yield movements correctly. We believe recent movements reflect growth and/or inflation concerns, not volume concerns. There are no bond vigilantes in the US or other currency issuing sovereign nations. The size of a government’s deficit (the number of tickets issued) is always matched by the non-government increase in savings pool. There is always enough money to buy the bonds.

While it can be tempting to fret over the 'cost of capital' for listed REITs, the reality is that long term real estate prices track replacement cost. An in a world where many real estate sectors are trading below said cost, falling supply and a shift in landlord pricing power matters more over the long term.

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.

1 https://en.wikipedia.org/wiki/One_Big_Beautiful_Bill_Act#:~:text=The%20One%20Big%20Beautiful%20Bill,debt%20over%20the%20next%20decade

2 https://www.theguardian.com/us-news/2025/may/22/what-is-trump-big-beautiful-bill

3 https://www.cbo.gov/faqs#:~:text=CBO%20typically%20updates%20its%20baseline,baseline%20produced%20in%20the%20spring.

4 https://live-aia-web.pantheonsite.io/resource-center/abi-april-2025-billings-continue-decline-architecture-firms