Real estate - still missing out on the recent recovery

In June, we provided an update on the real estate market and some early observations regarding the impact of COVID-19.

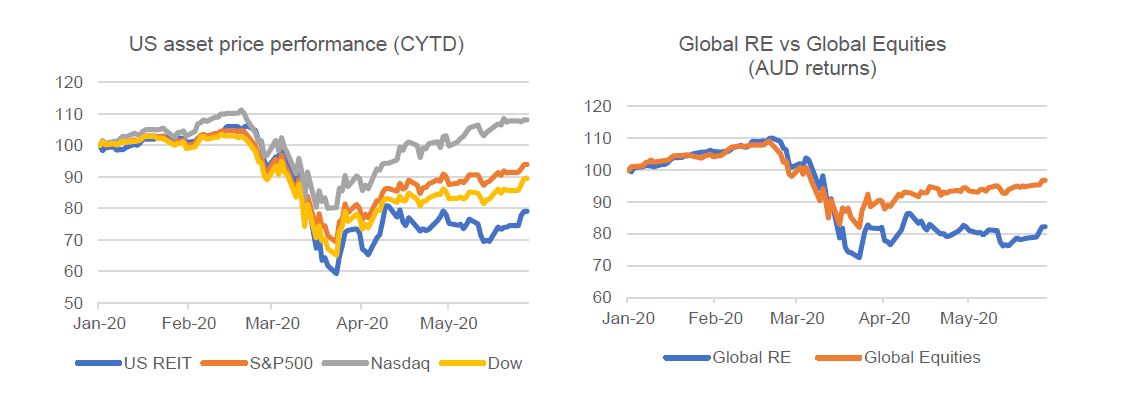

At the time it was clear the broader equity markets (US and global) were improving, while listed real estate was lagging. We have reproduced the June charts below.

Source: Bloomberg, Quay Global Investors

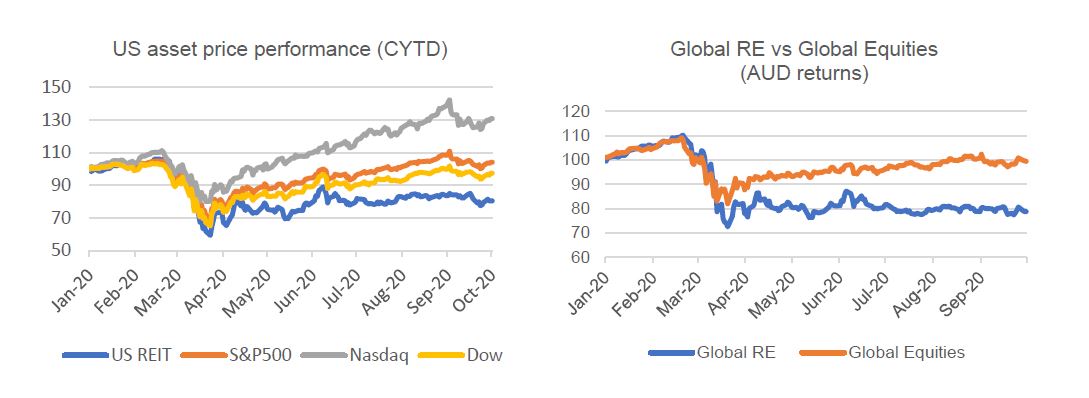

Since June, the equity rally has either continued (tech) or consolidated (equities), while listed real estate continues to lag in relative terms.

Source: Bloomberg, Quay Global Investors

As discussed in June, there are some easy narratives. Certain asset classes have been hit particularly hard (retail, office), but others have flourished (industrial, single family homes, data storage). The relative performance is hard to reconcile since the mix of winners and losers appears no different than broader equities.

Or is it?

Are there more ‘loser sectors’ in real estate compared to the S&P 500?

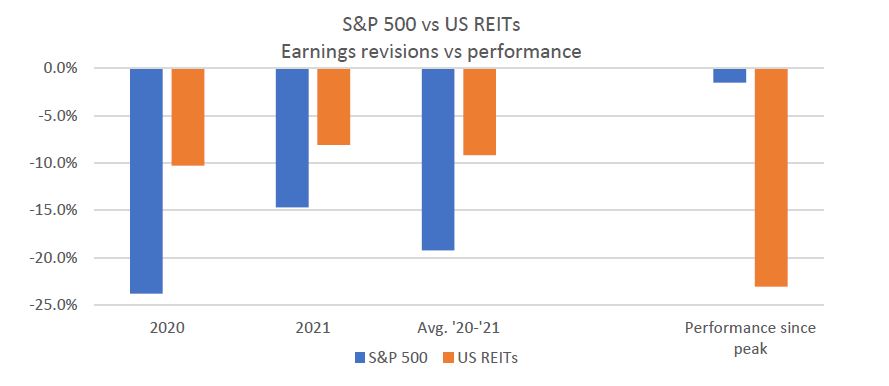

One way to test is to compare the size of earnings revisions since the impact of COVID. Using consensus data from Bloomberg, we note the average EPS downgrade for the S&P 500 (from February to September) is -23.8%, compared to real estate -10.3%.

However, a case can be made that the earnings impact on real estate is subject to a lag due to the prevalence of fixed leases in certain asset classes. For example, office sector rents may be falling today, but that will not impact earnings until leases expire or renew.

But even looking beyond 2020, average annual negative earnings revisions for real estate over the three years to 2022 (-8.0%) compares favourably to US equities (-15.9%).

From an earnings perspective, real estate is proving to be a resilient asset class compared to equities. This should come as no surprise. What is interesting is despite the earnings outperformance, listed US real estate has underperformed broader US equities by over 20%.

Source: Bloomberg, Quay Global Investors

Based on 2020 earnings, listed real estate has de-rated relative to equities by around 35%. We cannot convince ourselves this is sustainable.

Key elements across the sector remain relatively positive

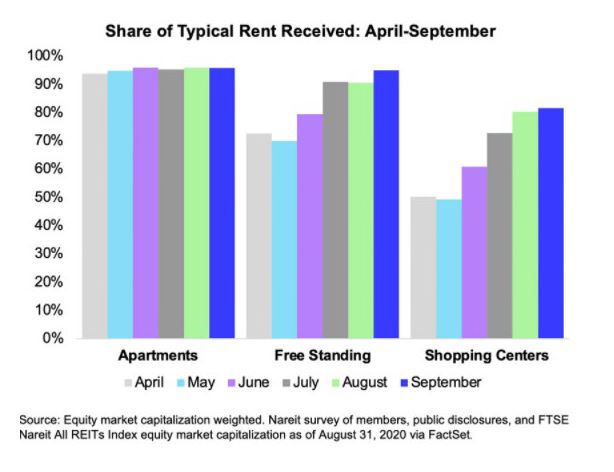

As we wrote in June: “One of the initial concerns stemming from stay-at-home orders was the inability (or unwillingness) of tenants to pay rent. Lack of rent would squeeze the cashflows of real estate owners, which (under a worst-case scenario) would lead to potential breaches of fixed-charge cover ratios within lending agreements”.

It was clear at the time that outside the retail and triple net lease sectors, rent collection was in line with historic norms. Since then, rent collection remains robust, and across the more challenging sectors, it’s improving.

Another observation from our June report was the current crisis is different from the GFC in that the credit markets remain open. Over the past two months, a few of our US investees have secured +10 year funding at ~2.0% per annum (S&P rating BBB / BBB+). In many instances the average cost of debt for our investees is 3.5-4.5%, suggesting material earnings tailwinds upon refinancing.

Of equal note is the availability of subordinated debt on incredibly attractive terms.

During the month, Scentre Group issued US$3.0bn (A$4.1bn) of subordinated notes for a term of 60 years at 4.75-5.12% per annum. The notes have no equity conversion, and compares to Scentre’s current average cost of debt of ~4.3%. The structure of the debt is such that 50% of the debt qualifies as equity for ratings purposes, and 100% as equity for covenant calculations.

Investors would be wise not to underestimate the value of this type of capital, and what it may suggest about the underlying investor appetite for yield.

Conclusion

For global real estate investors, the past few months have been frustrating as the sector continues to grind sideways while the broader equity market staged its incredible recovery – both in Australia and globally.

However, the relative price performance is at odds with the underlying fundamentals as measured by earnings. Moreover, near-term metrics for real estate (rent collection and credit availability) remain solid. Longer term, the sector can expect to enjoy material tailwinds from lower debt costs, and a reduction in new competitive supply.

The Quay Global Real Estate Fund remains fully invested.