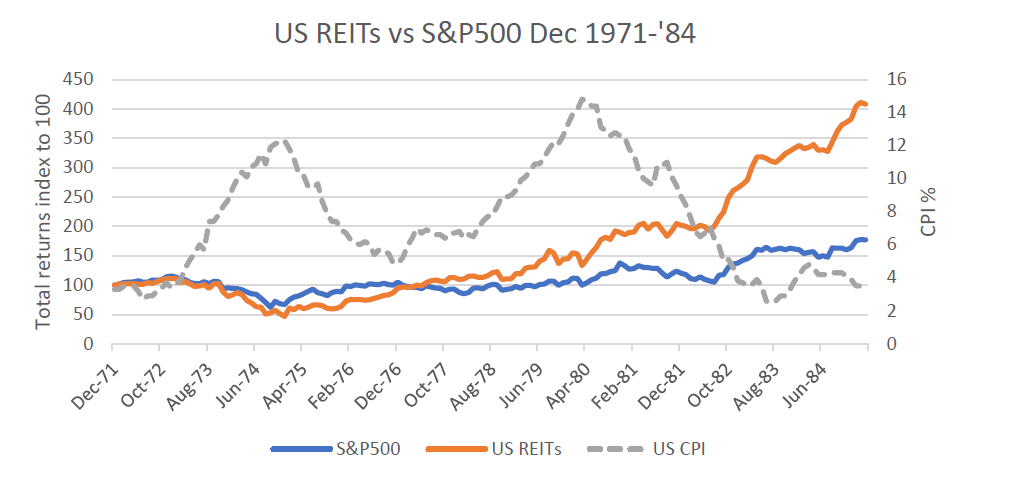

Source: NAREIT, Bloomberg, Quay Global Investors

What is not clear is whether listed real estate outperforms during moderate (say between 3-6%) or higher levels of inflation (say +7%).

While these levels of inflation may seem rare, the fact is that over the last 50 years US inflation has been above 3% more times than below. And during such periods, the nominal returns for listed real estate have been higher than low inflationary environments; and relative to equities, higher in both nominal and real terms.

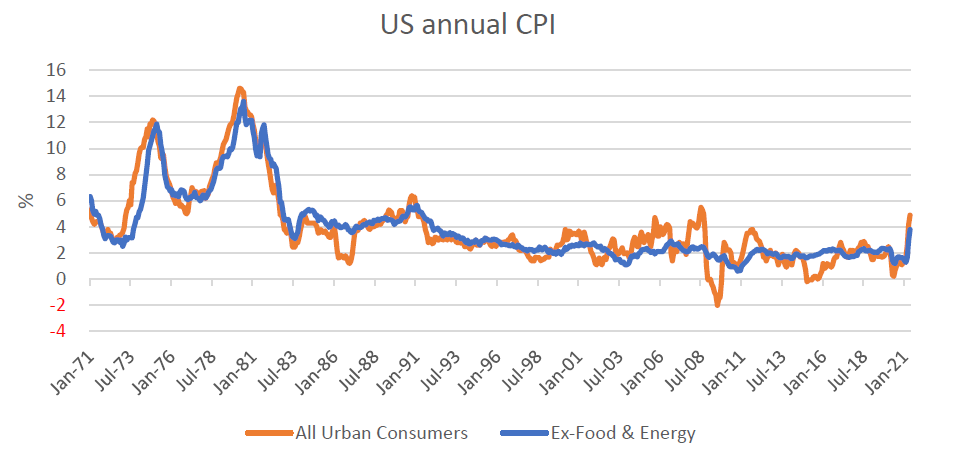

The rise and rise of CPI

Anecdotally, we believe real estate – and thereby listed real estate – to be a good inflation hedge. Land is tangible, and well-located land has an intrinsic value in that it can be used as a place to build shelter or as a place to do business or access services. Because of supply constraints, well-located land will generally appreciate over time. In addition, the cost of replacing any improvements built on the land will also increase through inflation. This is important, because if there is excess demand for a type of real estate, the market will have to accept rising costs and thereby the rents required to economically justify construction – regardless of the inflation environment.

Last month saw the US Bureau of Labour Statistics (BLS) release CPI for June (see following chart). For the last 4 months it has continued to rise and is now at a 5.4% 12-month increase, which is the largest such increase since the heady days before the GFC in August 2008. And if we exclude volatile food and energy prices from this headline number, while the absolute level is lower it is now the highest CPI print for this adjusted series since November 1991.

Discussion around the impact of rising inflation on investment returns is now firmly on everyone’s lips.

Source: US Bureau of Labor Statistics

There are pundits that believe this is cause for concern for the bond market, the stock market and the US dollar. All three could have an impact on our portfolio returns, but a lot will depend on whether this inflation is transitory in nature or not. We have previously published our thoughts on the debate here.

Regardless, it is worth understanding how listed real estate has performed in previous periods where inflation has been elevated. More specifically, at what levels of inflation does real estate perform best? Can there be too much inflation? Not enough inflation? What if the current US bond yields are correct (currently 1.2% per annum) and we are headed for sustained low inflation?

What it means for real estate

To examine the impact that different levels of inflation have had on listed real estate, we have looked at the returns over the last 50 years in absolute and real terms, and relative to general equities. Because global real estate indices don’t go back this far, we have instead used US REIT data and compared it to the S&P500. In our opinion, this represents a good proxy for listed global real estate given the large size and diversity of the US REIT market and also that it represents greater than 50% of the global sector.

The methodology was to analyse US REIT and S&P500 real and nominal returns by constructing indices for when headline CPI was both less than and greater than 3% and in increasing increments of 1%. From these indices the average monthly nominal and real returns could be calculated for the purpose of comparison. A summary of this output is highlighted below.

|

CPI Threshold |

Number of Sequences |

Months Total |

Max Months in any Sequence |

Avg. Monthly Return REIT (Nominal) |

Avg. Monthly Return S&P500 (Nominal) |

Avg. Monthly Return REIT (Real) |

Avg. Monthly Return S&P500 (Real) |

|

<3% |

17 |

282 |

110 |

0.8% |

0.9% |

0.6% |

0.8% |

|

3-6% range |

22 |

210 |

41 |

1.2% |

0.5% |

0.9% |

0.2% |

|

>6% |

4 |

103 |

66 |

0.7% |

0.0% |

-0.1% |

-0.7% |

Source: US Bureau of Labor Statistics, NAREIT, Bloomberg LLC

The results show that listed real estate is an excellent hedge for inflation and has historically delivered strong positive nominal and real returns in higher inflationary environments. It also offers a better relative return when compared to general equities. This is especially so when inflation is in the moderate 3-6% range, where listed real estate has historically generated more than double the real return relative to equities. Even with very high inflation (>6% and above), listed real estate continues to outperform equities (albeit at a lower relative level than in a moderate inflation scenario).

It’s also interesting to note that over the last 50 years, inflation has been above 3% more often than below. When it has been below 3%, listed real estate nominal and real returns have been quite a bit lower than in a moderate inflation environment. And contrary to common belief, in lower inflation settings listed real estate returns actually tend to lag equities.

Concluding thoughts

What can we conclude from this analysis?

Don’t fear inflation. In fact, when investing in real estate, inflation can be your friend. Higher inflation will protect your investment from supply issues (and therefore competition for tenants) and will drive up the replacement cost and residual value of your improvements. We have long argued that for most real estate, the ultimate anchor for value is replacement cost – and rising replacement costs are good for real estate. It is why replacement cost analysis is an important part of our process.

What is equally important is that a low inflation environment (<3%) tends to be relatively more favourable for equities (compared to listed real estate). This data cuts against the common narrative that low interest rates, and therefore low inflation, are better for property.