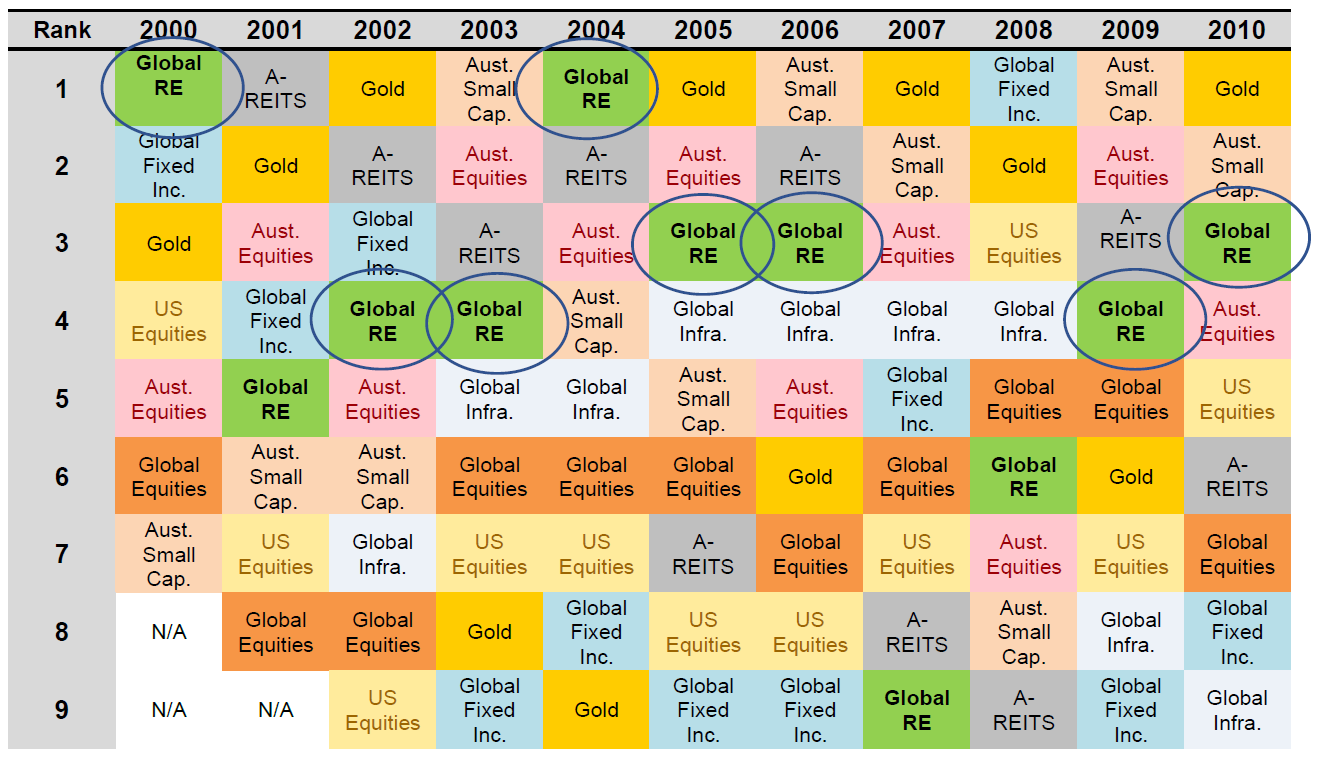

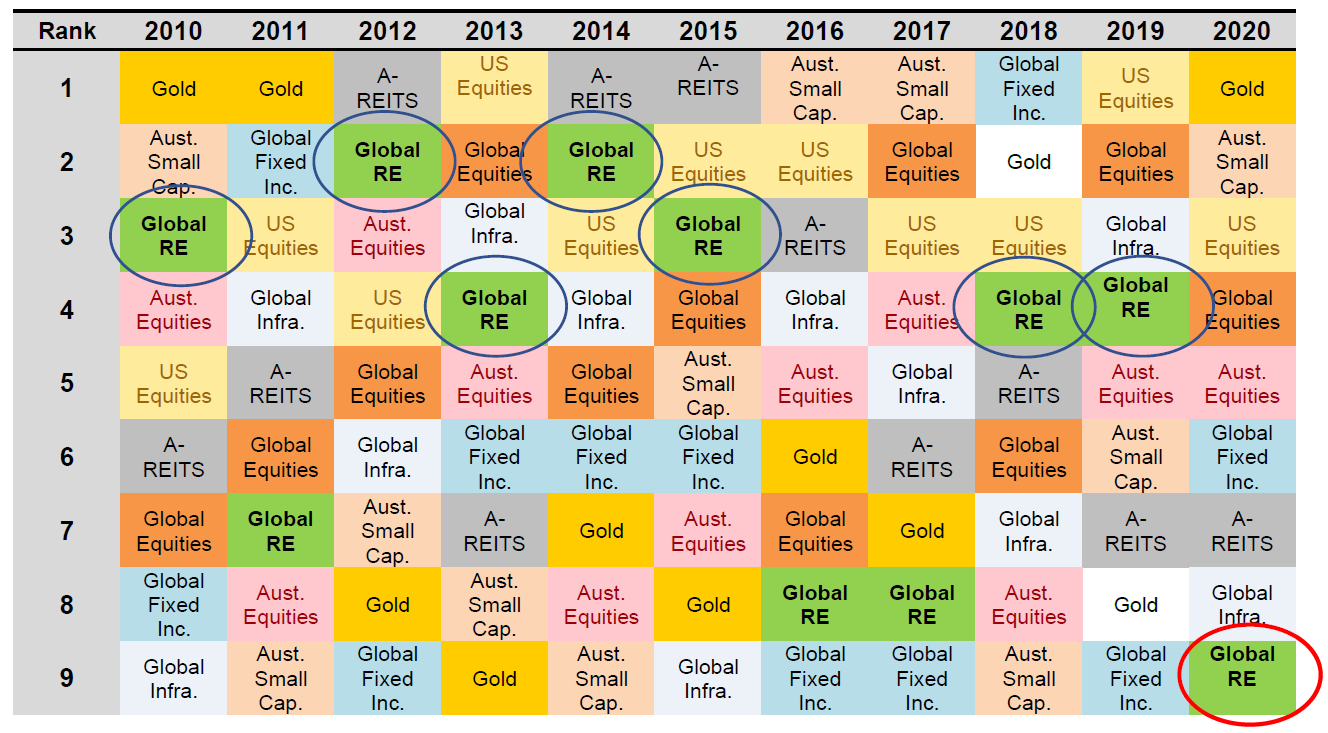

Total return (AUD) by sector by calendar year

Source: Bloomberg, Quay Global Investors

Notes: Global Infrastructure: S&P Global Infrastructure Index Net TR, Global Property: FTSE EPRA NAREIT Dev TR, Aust, Equities: S&P/ASX200 Accumulation Index, US Equities: S&P 500 Total Return Index, Gold: Spot Gold, Global Equities: MSCI World Index, Fixed Income: Bloomberg Barclays Global Treasury Total Return Index, A-REIT: S&P/ASX 200 Listed Property Fund, Aust Small Cap: S&P/ASX Small Ordinaries Index

Some asset classes and sectors performed well. Some, including global real estate, lagged. As most risk assets continue to spiral ever-upwards and relative performance becomes even more stark, we thought it was a good time to think about various asset classes, their performance, and some historic perspective.

In prior publications, we have referred to the ‘return quilt’, which has been ranking nine risk asset classes each calendar year since the beginning of the century. The returns are all in Australian dollars (see previous tables).

In 2020, based on our select group, Gold was a clear winner, along with Australian small caps, US equities (tech driven) and global equities. At the other end of the spectrum, domestic listed real estate (REITs), global unhedged infrastructure and unhedged real estate performed poorly.

As discussed in recent monthly performance reports, the underperformance of listed real estate is very much a function of direct government intervention, relating to certain ‘codes of conduct’ and moratoriums on tenant eviction.

However, taking a wider perspective of asset class performance by year highlights that sectors that perform poorly in one period rarely continue that underperformance. Of course, mean reversion plays its part; however, it is worth remembering that over the past 21 years:

- Global real estate finished the year in the top four for 15 of 21 years

- This compares to the much more popular global equities (5), Australian equities (10), and US equities (12)

- Global real estate and domestic REITs ranked highest on six occasions

- Compared to global equities (zero), Australian equities (zero), US equities (twice)

- Although global real estate has ranked low in prior years, the sector often recovers over the following years, ranking among the highest in the selected peers

- Global real estate ranked relatively high during the recovery years of the GFC (2009-2012) and the ‘tech wreck’ (2002-2004), belying the idea it is a ‘late cycle’ asset class.

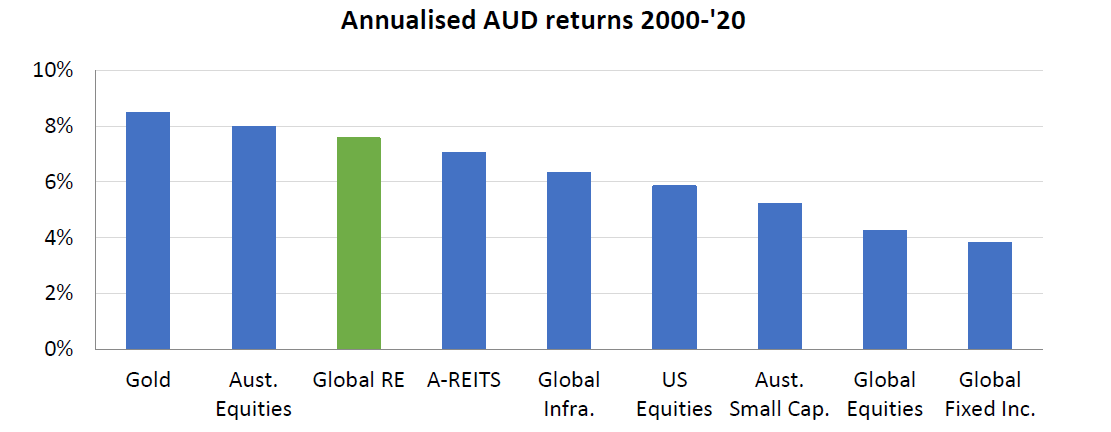

The accumulation of these observations is that global real estate total returns (unhedged) have delivered a credible performance so far this century.

Source: Bloomberg, Quay Global Investors

These returns should also be viewed in the context that over the past 21 years, real estate has disproportionately suffered through a pandemic and a (admittedly self-induced) financial crisis.

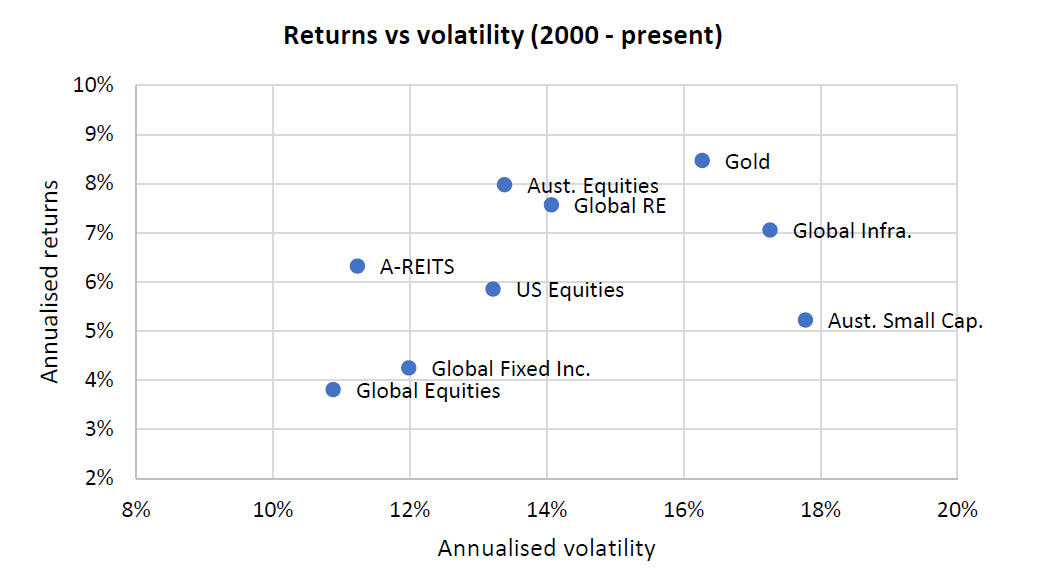

Dimensioning these returns against volatility (a crude measure of risk) suggests global real estate ranks mid-level. So, while investors may have to stomach more volatility compared to, say, global equities, they get compensated for that risk.

Source: Bloomberg, Quay Global Investors

Other general observations

Critics of this paper may suggest that since 2000, listed real estate has had an unfair advantage compared to other asset classes due to the steady decline in interest rates. However, as we have previously written, listed real estate is not particularly correlated to interest rates over the long term. In fact, the recent recovery in global listed real estate has coincided with a steady increase in bond yields.

Another argument is the potential impact of moving from a low inflation environment (2000-2020) to high inflation (+2021?). However, historically REITs significantly outperform equities during periods of high inflation.

The last half of the 2020s have been the worst period for global real estate, which can largely be explained by the sharp decline of retail property values since 2016 (retail accounted for almost 30% of the global index in 2015). This sector headwind is now behind us (as it is just 14% of the index today), and in some cases there are real opportunities in retail.

But the overall lesson is the same as with most forms of investing: patience. It can be tempting to allocate to sectors that are currently performing well, but when it comes to global real estate, mean reversion and a proven high-quality asset class means good relative performance is likely in the years ahead.