For this reason, when we launched the Quay Global Real Estate Fund in 2014 we didn’t set our benchmark to an index. Beating an index but losing investors’ money is never a good outcome. Instead, our investment process and benchmark is framed around beating inflation by 5% per annum (for more on the rationale behind that number, read our previous piece Benchmarking total returns).

Markets were roiled in February as investors worried that higher wages will lead to accelerating inflation. Bond yields acted accordingly.

So, if higher inflation was to return, how would we (and real estate) perform? Could a 5% real return be achieved in a high-inflation environment?

New year, same news?

The beginning of the calendar year brings with it the usual commentary: ‘interest rates will normalise’ and ‘the bond cycle is ending’. We heard this during the so-called ‘taper tantrum of 2013’, again in 2015, 2016 and of course last year. So is this year any different?

Well, maybe it is.

For the first time in seven years, all major economies are in synchronised growth. Indeed, the IMF recently increased its global growth forecast to 3.9% for 2018 and 2019, boosted by the sharp increase in the US fiscal deficit (tax cuts). An increase in the fiscal deficit is more akin to ‘money printing’, unlike quantitative easing which is really just an asset swap. The recent tax cuts will have some inflationary impact.

The environment feels like inflation should return; indeed, in some parts of the US economy it already has. Last month we highlighted the steady rise in construction cost inflation in the US, as per the following table.

This corresponds with direct company feedback that more developments are becoming difficult to ‘pencil’ as building costs are rising faster than rents. This causes development yields to fall, reducing capital availability and therefore reducing new supply.

But the issues in construction may be industry specific. Our analysis shows the capacity of the US construction industry has reduced significantly since the global financial crisis. This makes sense. Any individual entering the workforce in 2009-2011 would not be attracted to an industry that just imploded. Rolling forward to 2017, the industry is now short of (skilled) people, and capacity to build is constrained. We now have a real estate cycle where supply is elevated but not extreme – however, there is limited ability to add more from here.

In the residential market the situation is more dire. Total employment in residential construction is lower today than in 1999 – and as a percentage of total employment (that is, adjusting for the size of the economy) it is the lowest since 1992 (post-recession), as the following charts illustrate.

The construction industry is tight and experiencing cost inflation. This is good for real estate.

However, looking at the wider labour pool, it seems clear that there remains some slack in the US labour market – even at a low unemployment rate. The following chart highlights the employment-to-population ratio for the 25-54 year-old cohort, a key working demographic. The data shows that despite improvement in the labour market, there remains additional capacity in this worker pool that may limit wider inflation.

But what happens when this pool of labour is exhausted? What happens to real returns if inflation accelerates in a meaningful way?

Real estate vs equities: the impact of meaningful inflation

2018 may be the year accelerating inflation finally returns. If it does, what does it mean for listed real estate?

First, the US Federal Reserve may accelerate the rise in interest rates. In the short term, this could have negative consequences for listed real estate as unsophisticated investors may sell REITs in a knee-jerk reaction to abandon ‘interest rate sensitive sectors’. We have seen some of this play out already this year. However, in our paper Rising US interest rates, a headwind for REITs or equities? we highlight that US REITs significantly outperformed equities during the three-year rate hike cycle of 2003-2006. This coincided with relatively higher inflation at the time (circa 3% per annum).

For longer-term investors, rising inflation is unequivocally good for real estate. It drives higher levels of replacement cost, which underwrite current values and ensure new supply (when needed) will occur at a progressively higher price. This is why real estate has a reputation as one of the best asset classes to protect against any erosion of purchasing power (a key element of our investment objective).

If this sounds too theoretical, let’s turn to the data.

Listed US REIT performance during high inflation

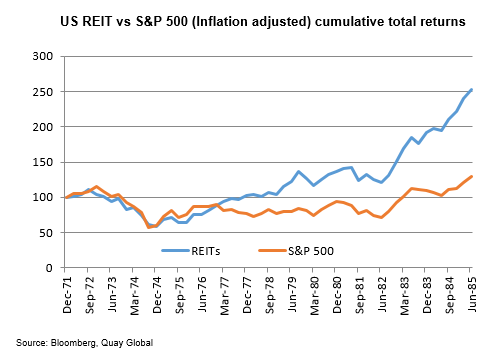

The poster child of higher inflation in recent times is the 1970s and early 1980s. Between 1971 and 1985 the average US inflation rate in the US was 7.6%[1]. After 1985, peak inflation never reached these levels again, and has since been an average 2.6% per annum.

So how did REITs perform during this period?

During periods of high inflation, listed real estate did an outstanding job protecting the real purchasing power of investor capital. Indeed, after adjusting for inflation, listed real estate delivered a total real return of more than 150%, or 7.1% per annum – well above our benchmark of 5%.

Equities preserved the real purchasing power of savers, as the S&P 500 delivered a real 1.9% return per annum – a significant lag relative to real estate.

As discussed earlier, the ‘cost-push’ effect on replacement cost underwrites higher real estate prices over time, so this outcome should not be a surprise. The fact that REITs performed in line with equities for the first 5-6 years highlights that it can take time for progressively higher building costs to reduce new supply and ultimately push higher real estate prices. Real estate is a long game.

However, the relatively poor performance of equities probably requires more explaining.

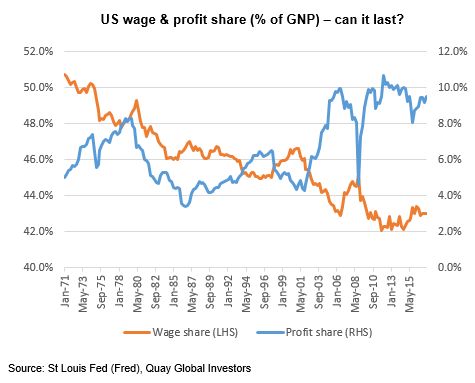

One of the largest costs for most businesses is labour. A shift in higher wages can affect margins, especially for businesses that have little product differentiation and are unable to pass on higher costs. This shift in ‘wage share’ in favour of labour crimps corporate margins – which at the same time underwrite higher real estate values. So the outperformance of the 70s-80s makes sense.

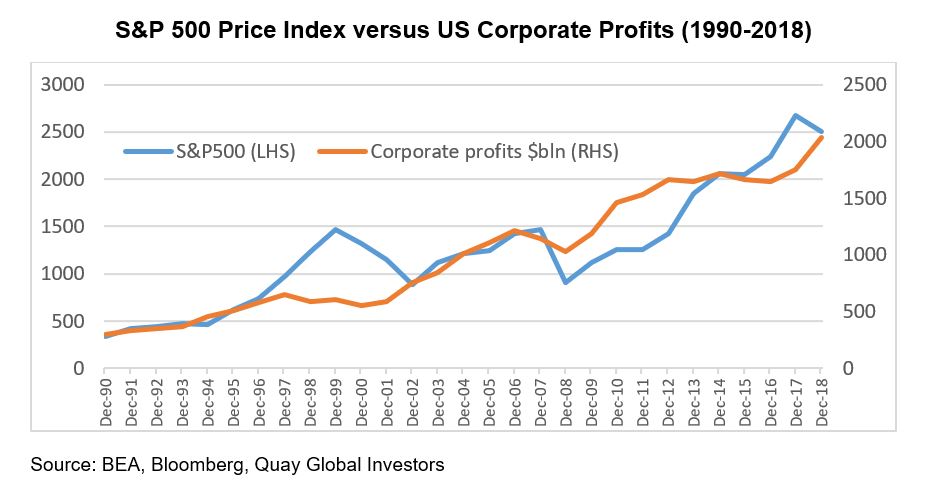

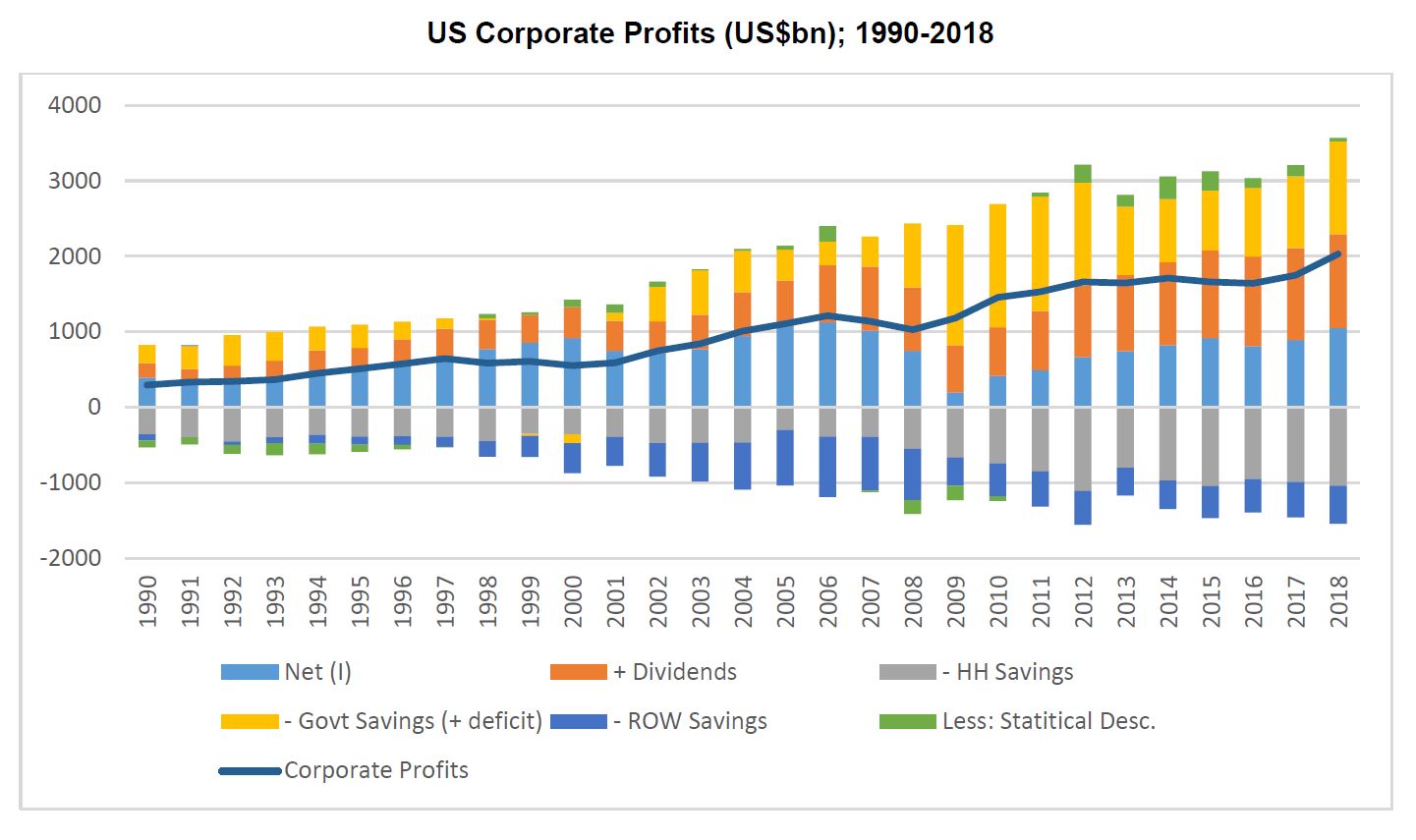

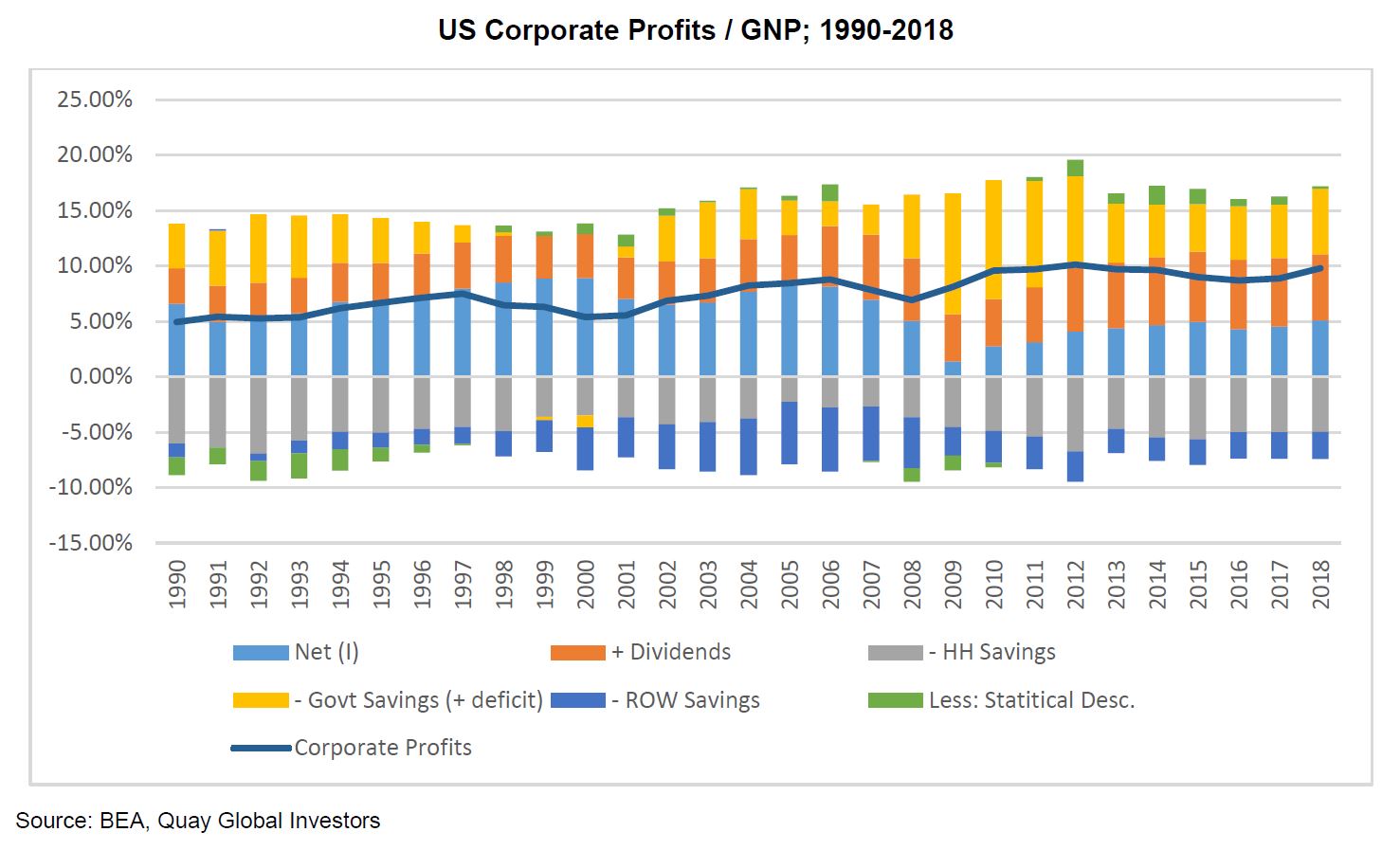

More recently, however, the booming US share market has come at the expense of wage share (i.e. the opposite of the 70s-80s), as shown in the following chart. This has been a great outcome for the owners of capital. But if meaningful wage growth returns and is sustained (which many central bankers and some politicians are hoping for), the outcome for owners of capital may not be so pleasant – falling margins with higher bond yields. The bad news for equity investors is the decline in corporate margins at the expense of higher wages feels inevitable – if not, who is left to buy the output?

In conclusion

On the back of recent wage data, the ‘bond bears’ are back – calling for higher bond yields and higher inflation. The knee-jerk reaction from inexperienced investors and equity managers is to ‘sell yield’, which invariably means REITs.

But higher bond yields, if sustained, can only be due to higher inflation expectations or higher real return expectations. If it turns out to be the former, listed real estate is likely to preserve and grow capital in real terms as higher construction costs underwrite higher values over time.

But what about higher discount rates – surely this reduces the net present value of future cashflows and therefore current share prices?

While it sounds counter-intuitive, for real estate valuation it doesn’t matter where bond yields are in 10 years. If it costs $20,000 per square metre to build an office tower in Manhattan by the year 2028, then prices will be at or around this level. If higher inflation means it is closer to $30,000 per square metre, then prices are sure to follow, or supply is forever constrained. In this way, real estate ensures the protection of purchasing power. If purchased well (below replacement cost) and sensibly financed, it can deliver outstanding long-term real returns.

Meanwhile, in this scenario, corporates will fight among themselves in a tight labour pool and battle against rising wages and rents to maintain earnings. Across the three ‘factors of production’ of land, capital and labour, capital is the likely loser – a stark reversal of the past 30 years.

To be clear, we are doubtful that accelerating inflation is imminent. If it does happen, however, it will be an overwhelmingly positive outcome for long-term real estate investors.

[1] Source: Bloomberg