As important it is to seek a competitive total return, we also seek to minimise the risk of permanent capital loss. To be clear, this isn’t mark-to-market losses driven by sentiment and noise, but losses that arise from a permanent diminution of business value.

Our approach is truly index agnostic. We are indifferent to a securities relative weight in an index – we simply seek the best real estate investment opportunities that can meet our investment objective with the lowest possible long-term risk. However, that’s a simplistic way to state our objective. Clearly there is more to it than that.

Portfolio construction plays an integral part in our strategy. For an index aware manager, this may begin with an index (the global real estate index may have more than 300 constituents) and the manager then adds or deducts from the index weights based on relative conviction. This type of approach is easy to understand, and usually results in the largest companies dominating the top weights in a portfolio. For example, many global real estate portfolios will generally include Simon Property Group as one of the top securities – and it is no coincidence Simon is historically the largest REIT in most of the global indices.

But how does a high conviction index agnostic fund like Quay construct a portfolio? It’s not surprising we are often quizzed about our approach to portfolio construction, especially since we are significantly different to our peers (we have never owned Simon Property Group[1]). Beyond selecting stocks, how do we allocate weights?

How many stocks are too many (or too few)?

The starting point for portfolio construction is to define the number of securities the fund is prepared to own. The Quay Global Real Estate Fund has defined a range of between 20-40 securities. How did we arrive at such a range?

Portfolio construction always begins with the best investment idea. Initially, the portfolio comprises of one security with 100% weight. By adding a second security, we gain the benefit of diversification, but at the cost of diluting (selling part of) our best idea. Clearly, there is a cost-benefit for every stock that is added to the portfolio.

Why is diversification so valuable? Former US Secretary of Defence, Donald Rumsfeld, once said:

“Reports that say that something hasn't happened are always interesting to me, because as we know, there are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns – the ones we don't know we don't know.”[2]

Rumsfeld was referring to the war on terror, but we believe the quote is equally applicable to portfolio construction. No matter what level of diligence, there are always risks that are simply impossible to know and mistakes can be made. And there are risks that may be known, but are nearly impossible to control.

So the addition of a second security to ‘our best idea’ portfolio comes with a significant diversification benefit. No matter how strongly we feel about our best idea, there are always ‘unknown unknowns’. With a philosophy of minimising the risk of a permanent capital loss, the addition of a second security to our portfolio is clearly prudent.

The same can be argued for adding a third, fourth, fifth security. But at what point does the benefit of diversification outweigh the cost of diluting our best ideas?

Finding the sweet spot

Before we launched the Quay Global Real Estate Fund in 2014, we attempted to quantify this answer.

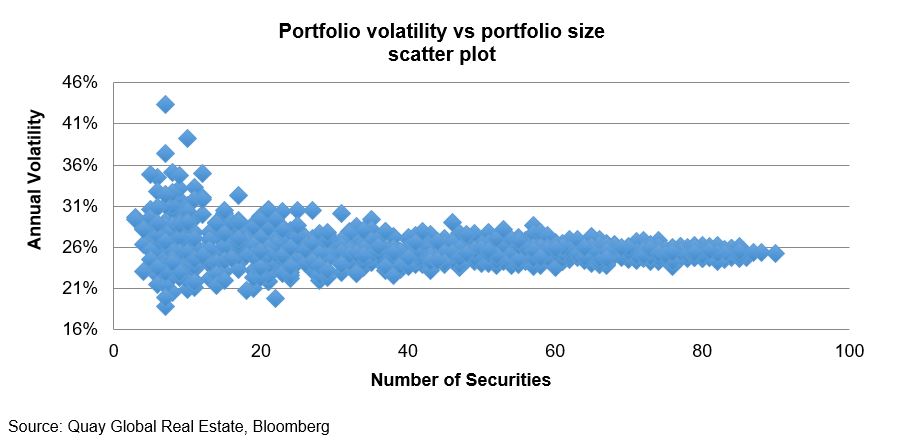

Using data between January 2009 and January 2013, we calculated and recorded the standard deviation of returns of 10 different portfolios of two randomly listed real estate securities. We then repeated the process for three securities, then four, and so on up to a portfolio of 90 randomly selected securities. In total we recorded the average volatility of 890 portfolios in total. The result was plotted as per the chart below.

By applying a ‘line of best fit’ to the data, we identified a clear pay-off diagram between measured risk on the y-axis (volatility) and dilution measured along the x-axis (number of securities).

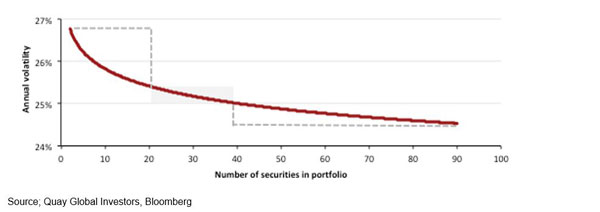

While our measure of risk is crude (volatility), the chart illustrates a point. The average difference in volatility between a two and a 90 stock portfolio is greater than 2% standard deviation points per annum. However, around half the volatility reduction occurred after just 20 stocks, and three quarters of the volatility is reduced with 40 securities.

Beyond 40 securities, the benefits of additional diversification are negligible – yet the cost (dilution) for additional securities is roughly the same.

At the other end of the spectrum, fewer than 20 securities begins to add meaningful volatility and we believe that for retail investors, the risk of fewer than 20 securities is too great.

Within this context, we concluded a portfolio of between 20-40 securities was optimal for our strategy.

Stock weights and defining conviction

The Fund also has a number of other hard risk limits, including the maximum individual and sector weights and minimum currency diversification.

Beyond these limits, stock weights are determined by conviction, which extends beyond simply the ‘highest returning’ prospect. We generally favour a lower return, lower risk opportunity compared to a higher return/risk.

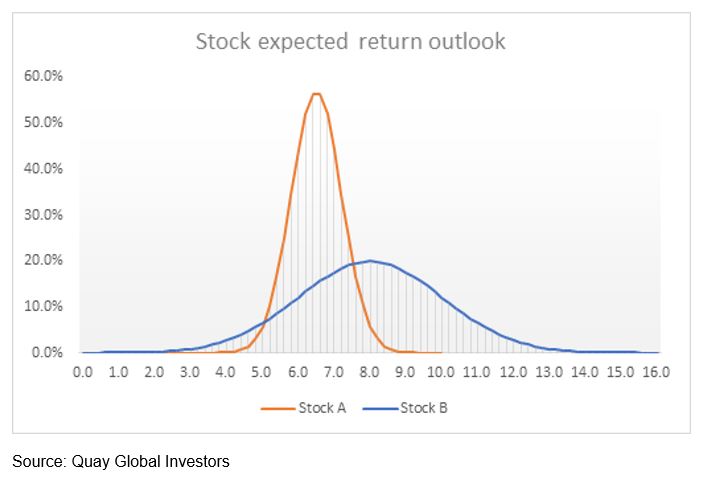

For example, consider the diagram below. It maps the expected return distribution between two securities, ‘A’ and ‘B’. Based on our expectation, both securities are expected to exceed our real return objective of 5% per annum (identified along the x-axis). But while B displays a higher expected return as measured by the median (8.5%), we would tend to favour and assign a greater weight to A (expected return 6.5%). This is because we are more focused on the left hand side of the chart (the risk of total returns falling below our investment objective) than the right (the risk of outsized returns).

In this example, the cumulative probability B’s returns could fall below our benchmark is 36.7%, while for A it’s just 11.2%.

Unfortunately, this type of analysis is prospective in nature. There is no statistical data that allows us to map the variance of returns as neatly as the chart above. However, through our fundamental research, detailed cashflow forecasts, sensitivity analysis and industry analysis we can form a view on the variability in our expected returns.

High conviction ideas: when to back up the truck

High conviction ideas must not only meet our return objective with a margin of safety (and have an assessed low distribution of returns), but they also have another characteristic – a skewed or asymmetric pay-off.

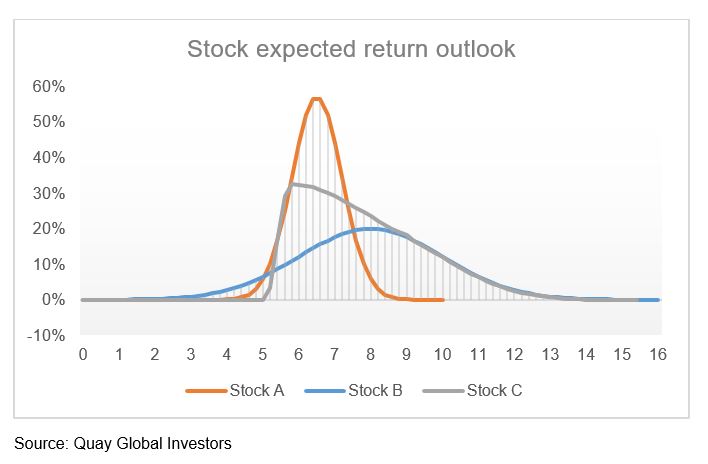

Consider the following chart. This time we have included security ‘C’, where the returns are skewed to the upside and the downside is limited. Of the three opportunities, C would represent our highest conviction idea and therefore the highest portfolio weight.

An example of these asymmetric returns could be a takeover offer, where the underlying security price is supported by a cash bid but there is the prospect of a higher offer. The downside risk is usually limited to the bid price, depending on the terms of the offer. But once a bid is public these are easy games to identify, so the upside is limited.

Longer-term, these scenarios also exist but are less obvious. Buying real estate at a substantial discount to replacement cost – or assets that are supply constrained and have a substantial barrier to entry or secular long run tailwinds (such as demographics) – also have very limited downside and skewed upside potential, but only if viewed through the prism of a long-term investment horizon.

Concluding thoughts

Regular readers will recognise recurring themes in much of our commentary. ‘Discount to replacement cost’, ‘demographics’ and ‘secular tailwinds’ are important concepts because they guide portfolio construction such that we can preserve capital over time, while hopefully delivering on our return objective (or better).

Quay’s investment approach is not a get rich quick strategy – we will always favour lower (acceptable) total returns with lower downside risk, rather than chase the ‘hot sectors’ of today that may promise higher returns but come with meaningful downside risk. It is this approach and philosophy that guides stock selection and portfolio construction.