“For long-term owners and investors it could be the right time to buy, as the market is pricing at a discount,” says Mr Bedingfield.

“The primary transmission mechanism of monetary policy is almost always via the housing market, which heightens uncertainty and risk for those looking to purchase property.”

During March there have been early signs the national property market is bottoming, led by Sydney.

“This should not be surprising, despite the strong belief that higher or lower interest rates drive the returns of residential property,” says Mr Bedingfield.

“The Australian residential property market’s best price gains have occurred without the influence of interest rate movements at all.

“We believe part of the recent recovery in dwelling values is driven by lack of available stock on market, as FOMO has been replaced by FORA, or ‘fear of renting again’. Despite the cash squeeze from higher interest rates, owners are likely to hold onto their homes to avoid the current brutal national rental squeeze.”

Mr Bedingfield says buying property during this period of falling property prices can be a good idea, especially if the purchase is for a principal place of residence. The best way to think about valuation is not to get too caught up with interest rates, but to purchase property below the cost to build.

“We believe that if you can buy a building at a discount to the cost to build, then you will be the first to make money once the development cycle kicks off again.

“As the population begins to grow again, property prices will have to get back up to building replacement costs, as this is the only way we will see developers start building again in a meaningful way.

“As long as it is sensibly financed and it's your principal place of residence, I think it's one of the better places to have your capital, but you do need to see it as a long-term investment.

“The reason I say principal place of residence is that it is tax-free and it's one of the last tax-free things you'll have. Even if you get an after-tax return on your principal place of residence of 3 to 3.5 per cent per annum, you will still do better than how global equities have performed over the past 20 years on an after-tax basis,” he says.

What about the so-called fixed rate mortgage cliff?

Mr Bedingfield suggests this is not as big a headwind as many suggest.

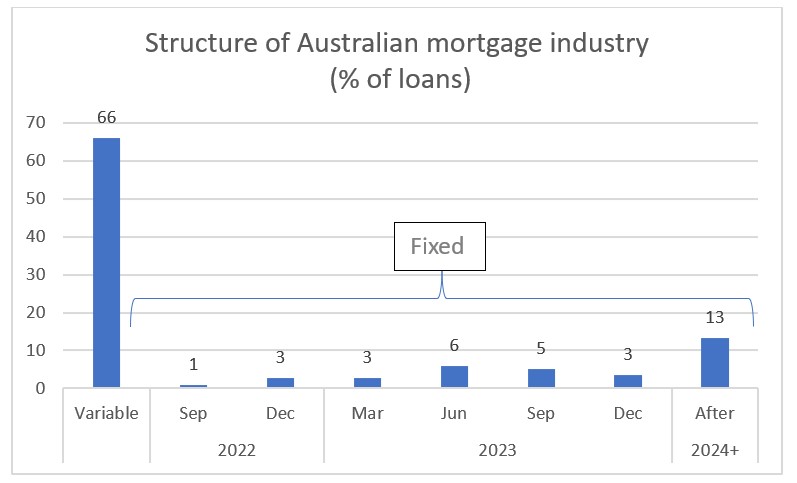

“The RBA estimates 34% of mortgages are currently fixed, half of which are due to reprice this year. That sounds pretty bad.

“However, the statement implies 66% of mortgages are floating and owners are already coping with higher rates. And despite this realty, stock on market remains still very low.

“Anyone expecting a surge in supply as fixed rates expire this year is underestimating the impact of FORA,” concludes Bedingfield.

Source: Bloomberg, RBA, Securities System, Quay Global Investors