Notably, after a post-COVID surge, Australian retail sales are beginning to slow. Indeed, for the March quarter, inflation adjusted retail sales retraced 0.6%.

As the data continues to show signs of weakness, there is a growing expectation that Australia faces its first real recession in decades.

REIT lessons from the 1990-91 recession

For many, the call for an Australian recession would include the expectation that shopping centers (malls) will bear a significant proportion of the downturn. After all, most malls are home to many discretionary retailers who will almost certainly bear the brunt of an economic decline as households tighten their belts.

Yet, such an expectation may not reflect the eventual reality.

No one under the age of 50 has ever seen first-hand the impact of a recession on the Australian share market. As such, any judgement around the performance of shopping centers based on ‘intuition’ during a recession may be misplaced.

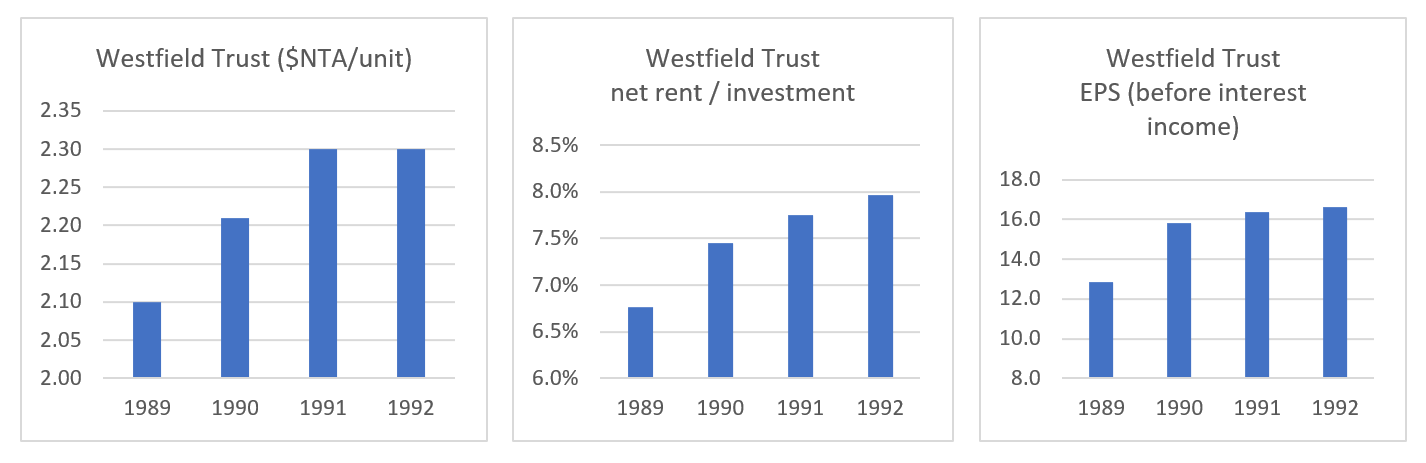

Fortunately, this writer was covering the listed REITs (known as listed property trusts) at the time. The overriding investing theme in the early 1990s was to invest in ‘earnings certainty’ – and at the time, that included listed mall REITs. And the go-to exposure at the time was Westfield Trust (the predecessor to today’s Scentre Group).

That may seem counter intuitive, however, equally fortunately this writer also retained many of the old annual reports of the Trust. The key financial ratios during this period (reproduced below) supported the ‘earnings certainty’ story that made the Trust an investor-favorite in the early 1990s.

Source: Westfield Trust annual reports, Quay Global Investors

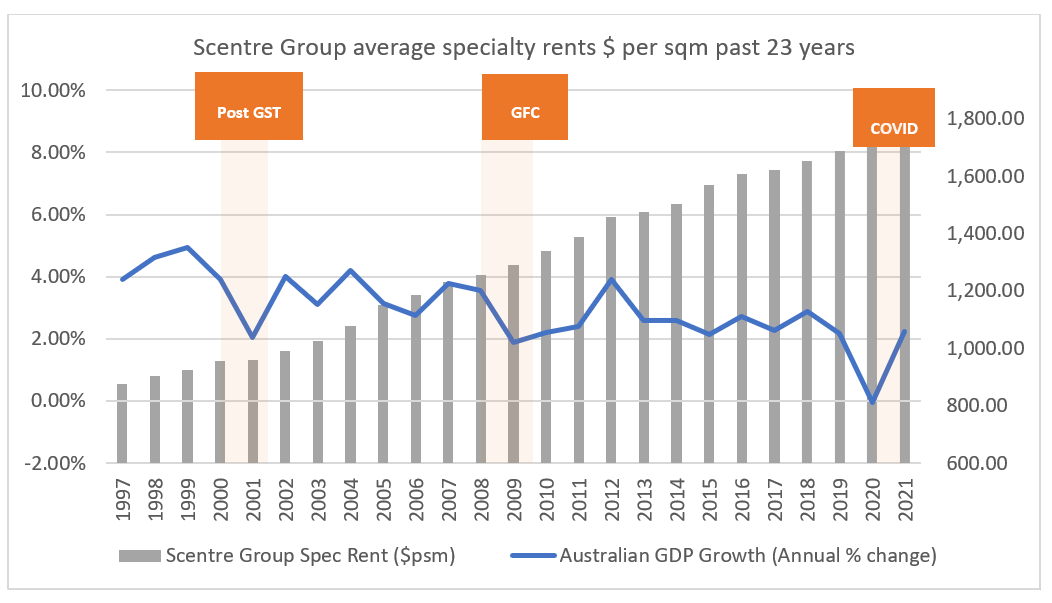

Long-term rental resilience

Australia has been fortunate to avoid significant economic downturns since the 1990-91 recession. However, national economic growth has not been without its bumps. The Asian financial crisis (1998), the post goods and services tax retail slump (1991), the global financial crisis (2008-09) and Covid (2020) have all presented economic challenges.

However, best-in-class retail rents have rarely declined, as depicted in the chart below.

Source: Scentre Group, Quay Global Investors

Of course, it can be dangerous to assume past performance is a guide to future performance. Much has changed in the shopping centre industry over the past 20 years. Household debt has ballooned, online retail is taking market share from stores, and consumer behaviour is always changing. Can retail rents maintain resilience as consumers become more cautious?

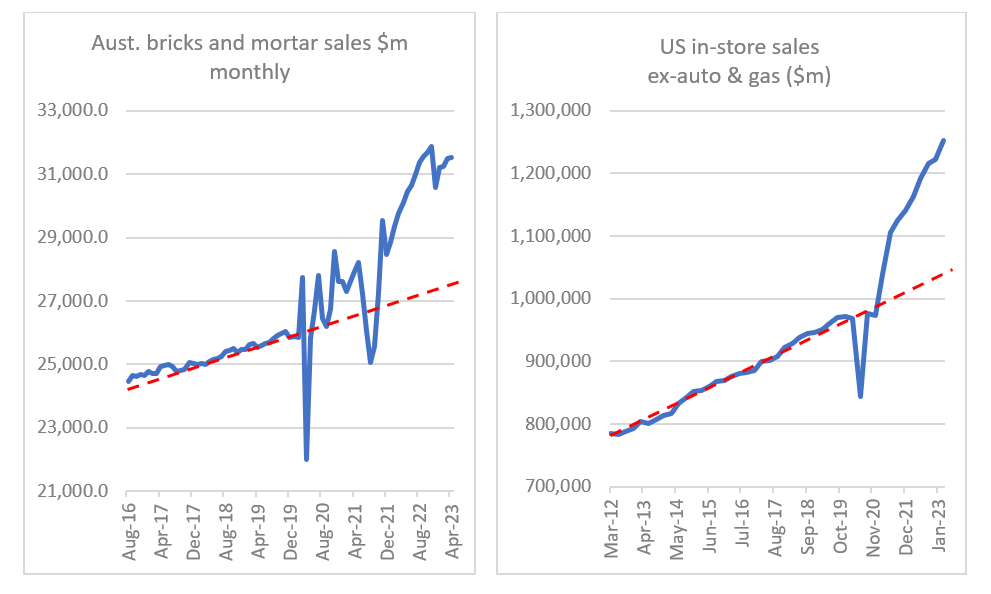

Store sales are well above trend

One advantage retail landlords have today is that in-store retail sales boomed post-COVID. And given most specialty leases are five to seven years in duration, rents have lagged economic and rental reality. This means most malls have passing rents below market rents.

In a recent Scentre group call, management indicated rent as a proportion of sales of specialty tenants is 16% compared to 18% pre-COVID. Or, said another way, retail sales can fall +10%, and the rent / sales ratio would reflect a normal pre-COVID world.

We see the same dynamic in the US.

Source: ABS, US Census Bureau, St Louis Fred, Quay Global Investors

NB: In-store sales derived from total system retail sales less reported ecommerce sales

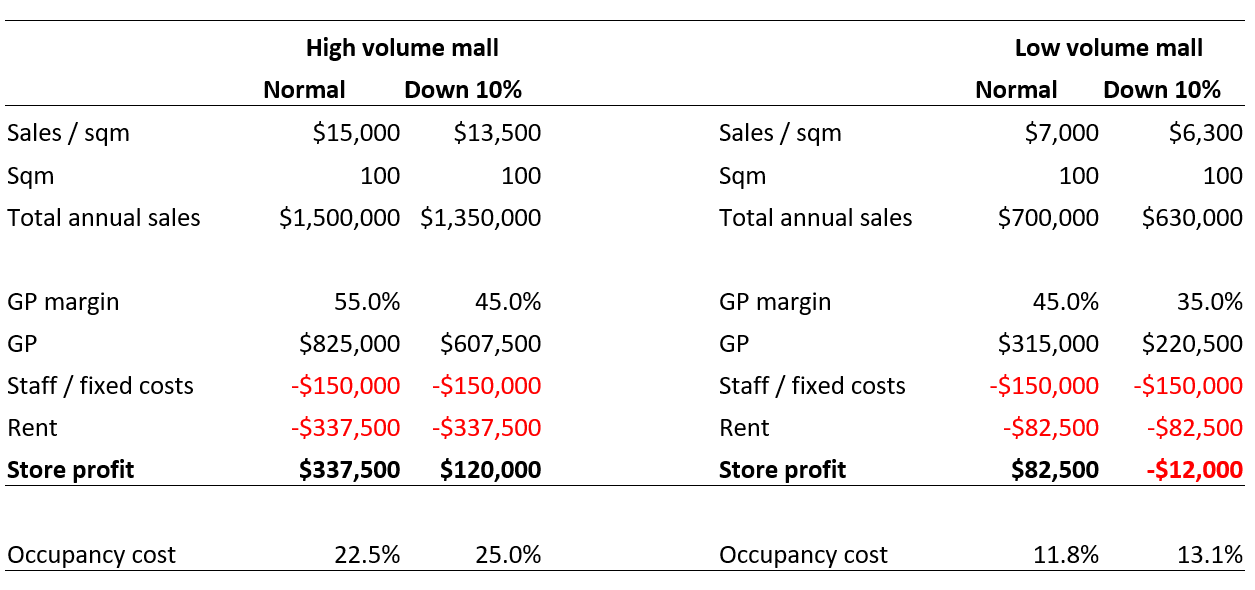

However, the best-in-class malls have another advantage. – which becomes apparent when analysing unit level economics of an average retail store.

In-store unit level economics

To be clear, not all shopping centres performed well in the early 1990s. Properties without scale and low sales productivity lost tenants, and income declined. Yet, it still seems a paradox that during a severe recession, the most secure investment was a regional shopping centre.

To understand these dynamics better, it’s useful to look at what happens to overall store profitability during a downturn.

Firstly, it should be stated that the vast majority of rental income from a shopping centre is from base rent (+95%), and therefore immune to short-term sales turnover. However, a sustained decline in sales can push tenancies to bankruptcy and/or a negotiated lower rent.

To understand the economic impact of a downturn, we present the table below where we analyse store profitability within two types of shopping centres – a high sales volume asset (specialty sales per sqm $15,000) and a mid-range low-sales volume asset (specialty sales $7,000). With some basic margin and cost assumptions, both stores are profitable in a normal environment.

Source: Quay Global Investors

In the event of, say, a 10% decline in retail sales, the high volume mall maintains its profitability even at the same level of rent, while low volume mall becomes unprofitable. During recessions, cuts need to be made, and in this scenario, the low volume store is unlikely to renew their lease, or at the very least, demand a rent cut.

When looking at the occupancy costs for both tenancies, this also seems counter intuitive. The retailer in the high volume mall has a significantly higher occupancy cost ratio (rent/sale) than the smaller mall (22.5% versus 11.8%). Since this measure is used to assess affordability, investors can be forgiven for thinking the mall with the lower occupancy cost is relatively immune to a downturn.

But the opposite is true. At the store level, the low turnover mall has a number of disadvantages:

- Generally lower gross profits margins and lower absolute gross profits (need more discounts to attract sales/ volume).

In 1990-91, vacancy rates in these malls increased, while the most productive malls maintained near full occupancy, and as the Westfield Trust financials highlight, maintained and grew rents while sustaining asset values.

How this impacts Quay’s investment approach

It has been over 30 years since Australia’s last deep recession, and it feels like some of the investment lessons have been lost in the passage of time.

While it seems intuitive to think retail landlords will disproportionally suffer a deep recession, history and analysis suggests these assets are likely to maintain profitability amid a seas of profits downgrades across the broader equity market. If the 1990-91 market performance is repeated, and a desire re-emerges to invest in earnings certainty, retail REITs may be the best place to be.