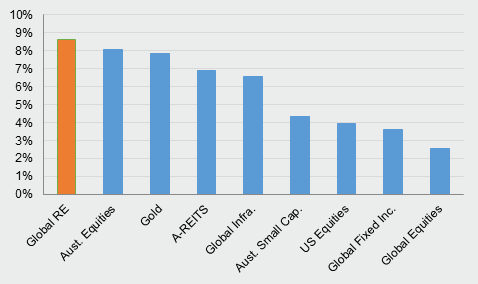

Property outperforms equities over the long term

Earlier this year, we spoke at the Bennelong Investment Forum. Our presentation included a number of charts, but for many, this one stood out.

Annual Total Returns (AUD) – 2000-2015

Source: Bloomberg, Quay Global Investors

On reflection, it could be argued that we were penalising equities, since our chart began as the dot-com bubble peaked in the year 2000. In a similar way, starting any chart from 2007 would also be unfair to real estate.

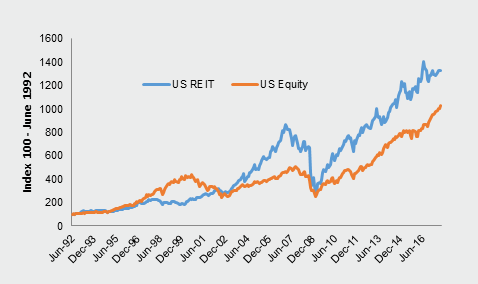

Consequently, we have extended the analysis back 25 years, as depicted in the charts below. The first chart shows cumulative returns for US listed real estate (REITs) against US equities (S&P 500) since 1992. While both perform ‘in-line’ for the first three years, indicating the starting point is giving no real advantage to either asset class, the longer-term relative performance speaks for itself.

US REIT vs US Equity Cumulative Return Index

Source: Bloomberg, Quay Global Investors

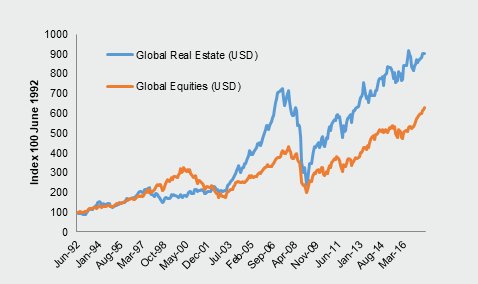

This is not just a US phenomenon. For global listed real estate, the results are similar.

Global Real Estate vs Global Equities Cumulative Return Index

Source: Bloomberg, Quay Global Investors

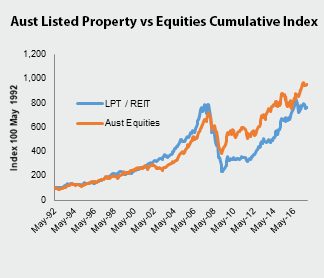

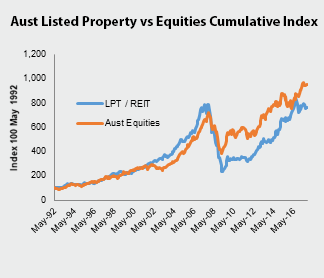

In Australia, listed REITs (formerly known as Listed Property Trusts) have not quite kept pace with equities, which is not surprising given the credit (banks) and mining (resources) super cycles. Having said that, direct residential property in Australia (as measured by a price index) has significantly outperformed Australian equities – much to the chagrin of many equity managers that have called the sector a bubble over the past 10 years.[1]

Source: Bloomberg, Quay Global Investors, ABS

The facts are in. Real estate tends to outperform equities over multiple cycles.

This is not a surprise to us, nor to the very wealthy who choose to store wealth in the form of land and property. The real issue is to explain what has been happening over the long term, and why real estate tends to outperform ‘growth’ equities.

Ignorance is strength?

We read most of the day. In fact, it is probably 99% of the job. We read as much as possible about our investees, their competitors and markets. We also like to read about long-term themes and businesses that sit outside real estate.

Sometimes we read other equity managers’ commentary, particularly if we believe they have interesting and useful insights that may indirectly assist our investment process.

What strikes us is the disdain some general equity managers have for property, from blaming real estate for the financial crisis (banks...?), to being wrongly categorised as a play on interest rates (see our Investment Perspectives article from December 2015 for the rebuttal).

Indeed, we recently read the view that ‘property’ (real estate), along with crypto-currencies, is currently part of what economist John Galbraith once described as “the bezzle”[2]. That’s cold.

But what’s really happening is nothing more than widespread ignorance about the asset class. Constantly labelling real estate a ‘bubble’ or ‘interest rate play’, rather than recognising it as a tried-and-tested store of wealth anchored to ever-increasing replacement costs, means a large pool of equity funds simply bypass the opportunity. This in turn leaves the asset class undervalued (and under-appreciated) relative to general equities, giving it plenty of room to outperform over time as the cashflows outweigh perception.

Equities are about ‘creative destruction’ while real estate simply maintains its share of income

We recently came across an article from the Wall Street Journal with an interesting statistic quoted:

“From 1926 to 2015 only 30 stocks accounted for 1/3rd of the cumulative wealth generated by the US Stock market; Amazon was one. That’s 30 out of a grand total of 25,782 companies that were publicly traded over that period”.[3]

Other observations from the article include:

- Just 0.33% of all companies that were part of the stock market over the past 9 decades accounted for over half of the accumulated wealth for investors; and

- The top 1000 performers over this period (4% of total companies) account for 100% of accumulated wealth.

These are incredible statistics, and we are not sure whether this fact supports active or passive equity management. What are the chances of finding the next Amazon, or the 1 in 25 company that will account for 100% of future wealth accumulation?

The fact that Amazon was one of the 30 stocks that accounted for one third of wealth accumulation since 1926 highlights the actual cost of owning equities – business obsolescence. It could be said that rather than creating wealth, Amazon has transferred it – from existing retailers and weak brick-and-mortar stores. Much in the same way, Apple, Samsung and Google have stolen the market from Eastman-Kodak, traditional media and other sectors.

But this is not new. Capitalism has always been about creative destruction.

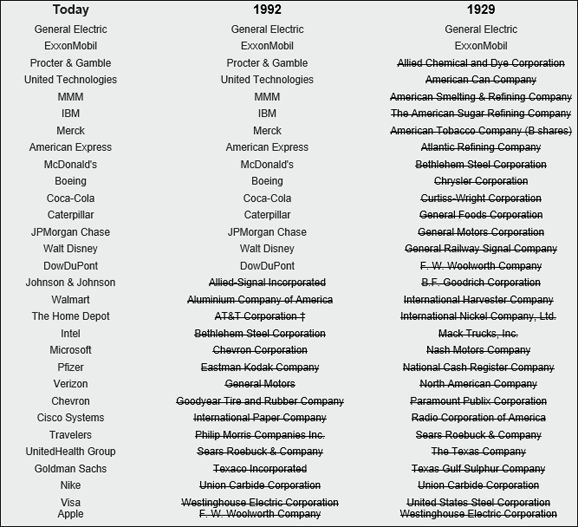

To illustrate the point, the following table shows the 30 constituents of the Dow Jones Industrial average today, in 1992 and 1929 (pre-Depression). Only half of the current constituents were in the index in 1992 (the start year of our performance calculation above), and only two were in the index pre-Depression.

That is not to say that the companies no longer in the index have not survived – many have. But many have also succumbed to the realities of capitalism – evolve or become obsolete.

Constituents of the Dow Jones Industrial average

Source: Wikipedia

In comparison, the rate of obsolescence across institutional quality real estate is remarkably low. Land located in New York, London, Tokyo and Sydney was valuable in the 1930s and is just as, or likely more, valuable today. There is no reason to doubt that well-located land’s claim on the economy will be relatively stable over time, as it will always remain one of the critical factors of economic production[4]. That is, land values tend to grow in-line with the economy, while the rate of obsolescence is virtually zero.

That is a massive advantage compared to the brutal and destructive world of capitalism, which via business obsolescence dilutes long-run equity returns – which brings us to our next observation.

Equity returns are not that exciting

Much has recently been said about the astounding performance of the US equity market since the depths of the global financial crisis. Since March 2009, total returns (USD) have exceeded 300%. However, long-run returns have not been as exciting. Since 1870, the long-run real total return from US equities has averaged 6.5% per annum.[5]

Moreover, long-run real earnings per share in the US has averaged just 2.6% per annum since 1953, and just 0.5% per annum in Australia.[6]

Don’t get us wrong – that’s still pretty good. But it is easy to see that well-located real estate growing in line with the economy plus a yield, enhanced with the benefit of moderate leverage, can compete with such returns.

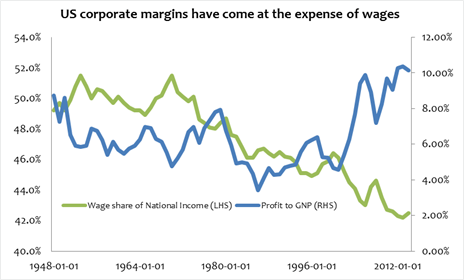

A case can be made that equity valuations look vulnerable from current levels – not only from a Price / Earnings perspective, but the massive tailwind of ever-increasing profit share will at some point end and possibly reverse (especially given the rise of populist politics).

Source: Federal Reserve Bank of St Louis, Quay Global Investors

How does this affect Quay’s investment approach?

Real estate (listed or otherwise) tends to be characterised as a ‘proxy for bonds’, a ‘yield play’ and a ‘defensive asset class’. However, for longer-term investors, the sector represents a store of real (inflation-protected) wealth—which, if carefully selected and financed, avoids capitalism’s brutality of obsolescence, which in turn provides the asset class with a significant advantage relative to equities over time.

While many investors’ investment portfolios are equities-centric—domestic or global—we believe such investors would be well-served to consider diversifying into global real estate.

Knowing global real estate has historically been a very competitive asset class from the perspective of total returns, in 2013 we believed an opportunity existed in the investment management industry. Relative to the number of equity funds available for investors, there was not as much selection across the global real estate universe. Moreover, of the global real estate funds available, many strategies were similar in nature.

We formed Quay because we believed better returns (and lower risk) were available for investors relative to the wider real estate indices as well as relative to other asset classes. Our conviction was that by identifying the best global investment propositions across an asset class, with a demonstrable and compelling track record, we could offer investors such an investment.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular, this newsletter is not directed for investment purposes at US persons.

[1] We recognise direct property indices are not always accurate, as they tend to understate (or exclude) maintenance capital expenditure. However, this chart is still biased against property as it compares un-leveraged real estate returns to leveraged equity returns.

[2] “That increment to wealth that occurs during the magic interval when a confidence trickster knows he has the money he has appropriated but the victim does not yet understand that he has lost it.” John Kay, The Financial Times, 22 October 2003

[3] Wall Street Journal, 16 May 2017

[4] Along with capital, labour and entrepreneurship

[5] www.pragcap.com/u-s-equities-long-term-real-returns, accessed 1 November 2017

[6] Quay Real Estate Advisors, Investment Perspectives: Benchmarking total returns, November 2014