Along with this discussion is the inevitable ‘get out of bond proxies’ hype. We have discussed in prior papers that empirical evidence does not support the idea that real estate underperforms during rate increases.

In this paper we are taking a more theoretical approach to the discussion, albeit backed by real life data and examples.

As part of our process, we seek to differentiate between commodity real estate assets and those which are franchise in nature. And while one of the risks of commodity assets is that they are more prone to (over) supply, we take that theory one step further and highlight how in the long-run, falling and sustained low interest rates can actually be detrimental to the long-term total return proposition, particularly for this type of asset.

When CPI linked rent increases do not equal CPI

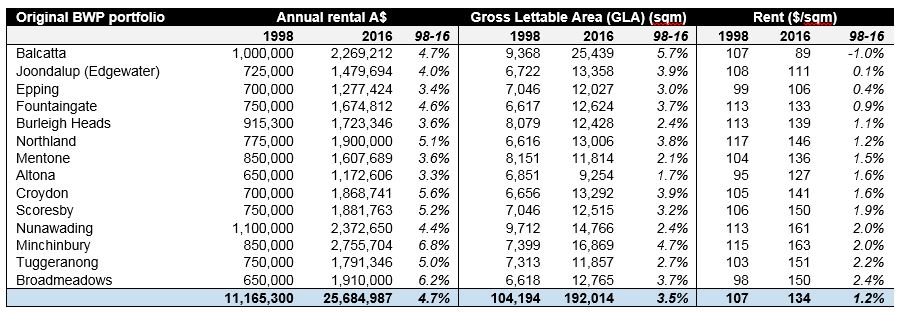

We were recently sent some interesting data from Credit Suisse relating to the Bunnings Warehouse Property Trust (now BWP Trust) highlighted in the table below. The REIT was listed in 1998 as the landlord for the Bunnings retail business selling home improvement and outdoor living products from large-format retailing properties in suburban locations. The leases were long term (10-15 years) and had annual rent reviews linked to CPI, with some market reviews included over longer time frames (+5 years). In most instances, the market reviews were well ahead of CPI.

Credit Suisse analysed the starting net property income (NPI) for each property and compared it to the NPI of the same asset today. The compound annual growth in income was 4.7%. However, over the same time frame, the rent/sqm only increased by 1.2%, well below inflation.

The rent was contracted to increase at CPI each year – and most market reviews have been well in excess of CPI. So how can this be?

The role of marginal return on capital

Over the 18 years analysed, each asset was expanded, on average, almost doubling in size.

The issue is that the new areas were built based on a feasibility with a much lower return on capital – thus diluting the rent/sqm progressively for each expansion.

Consider the following example.

Imagine a Bunnings Warehouse has the following financial metrics:

- GLA 10,000 sqm;

- initial rent at $100 /sqm;

- NPI = $1m (10,000 x $100); and

- purchase price = $10m (10% capitalisation rate) = $1,000 /sqm.

Now imagine after a number of years the size doubles to 20,000 at an incremental cost of $1,000 /sqm (incremental cost $10m) with a target yield on cost of 7%. This is lower than the initial yield because interest rates have fallen over time, and the trust can undertake the expansion and still be accretive to earnings per share.

Upon completion, the property is generating $1.7m per annum ($1m + $0.7m for expansion) or $85 /sqm. That is a 15% reduction in rent/sqm.

The lesson? Sustained lower return on capital employed – relative to history driven by low interest rates – means per sqm rents declined in real terms.

It’s not all bad news

This might sound like a disaster for BWP Trust unitholders. But the reality was that while rent/sqm declined in real terms, they benefited from a competitive marginal return on capital and therefore earnings per share increased. In addition, the dilution in rent/sqm was more than offset by lower property capitalisation rates (higher EPS multiple).

It’s not all good news either

BWP Trust unitholders offset the rent/sqm dilution by ‘capturing’ an attractive marginal return on capital. Overall value was created for unitholders.

However, this is not always the case.

Consider a commercial office building. Unlike a Bunnings site, office assets are very difficult to expand. When a developer adds a new office property in a CBD, the incremental return on development is captured by a third party i.e. the developer of the new building. And in a world of sustained low interest rates and falling capitalisation rates, the rent/sqm required to make new development feasible, will most likely, be lower than existing stock. And over a cycle, this will be (and has been) repeated time and time again, negatively impacting on the ‘market rate’ for existing office owners.

Ultimately, office owners face the long-term prospect of below inflation rent growth, without the benefit of any incremental return on capital. In fact, because of the high levels of depreciation, the actual rates of return will be much less.

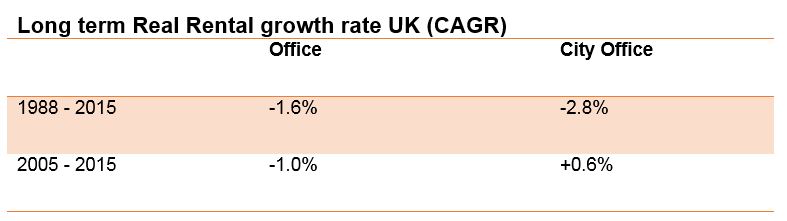

This is more than just theory – below is an example of real rent growth per sqm for London office – 1988 to 2015. A period where there has also been a secular decline in interest rates.

For an owner of an office building, this is not always bad news – the lower growth rate is offset by lower capitalisation rates generating capital gains and sustaining acceptable total returns even over several cycles. At least until interest rates bottom and cap rate compression ends. Without further cap rate compression, future total returns suffer.

In London, West End and City cap rates range around 3-4% and without further cap rate compression, which may or may not continue, investors are very reliant on long-term rental growth to generate attractive total returns. Who knows, maybe the next 10 years will be different for market rent growth? (Once we get through the supply under construction.)

The lesson is: when interest rates are low, look beyond the cap rate compression, as long-term rental growth may not actually meet your expectation.

Differentiating the asset classes

It is not just office property that suffers from this dynamic. Any commodity style property that is already fully built-out faces the same risk. This includes industrial, storage (self and data) and some residential.

Real estate that is hard to replicate, and / or provides opportunities to invest incremental capital at competitive returns, is well protected and remains an attractive investment prospect irrespective of the interest rates environment. That includes best in class retail, manufactured homes, on-campus student accommodation and health care (hospitals, post-acute care, etc.).

How does this affect Quay’s investment process?

When investing for short-term gains (absolute or relative) this dynamic is not relevant. But for long-term investing, it is important to understand the impact the macro-economic environment has on the overall total returns from the underlying real estate. Sustained low interest rates can be great in supporting low capitalisation rates, but may erode rent per sqm growth in real terms. For Quay, this is an important consideration given our investment objective is to generate a real rate of total return of +5% p.a. over the long term.

At Quay, we place emphasis on differentiating between commodities versus franchise property. We also play close attention to the marginal return on capital – which, if coupled with low payout ratios, can generate very attractive and sustainable total returns irrespective of the interest rate environment.