To reduce the unknown risk, we seek to build a portfolio that diversifies risk by currency, geography, stock and asset style. We also place weight on company management and leadership. Just as our investors seek to understand our investment philosophy and process, we try to do the same for our investees.

We hope future investors at Quay will invest based on our investment process, track record, experience and philosophy. We do not expect anyone to invest because we may offer our fund at a discount to NAV (we won’t).

We approach real estate investing the same way. While a discount to NAV (however it may be calculated) may prove tempting, we fundamentally believe buying a good business and sensible investment process will generate more sustainable attractive long-term total returns.

An equity holders’ CEO

We believe the Chief Executive Officer (CEO) is a large determinant of an investment’s long-term total returns. The CEO hires (and fires) senior management, sets and manages the strategic direction and culture of the firm and manages the conflicts that arise between various stakeholders in the firm. As equity investors, these things matter, however, insofar as they impact on the sustainable cash flows the business generates for shareholders. This paper looks at a good CEO from the equity holders’ perspective. So, what makes a good CEO?

One of our larger investment positions is the US Health Care REIT, Ventas Inc. We like Healthcare as a sector. The demographics are compelling. But near-term risks, particularly political, are real. Why did we choose to invest in Ventas? This is where an experienced CEO matters. There are plenty of other perspectives on what makes a good CEO, but we have decided to write about Debra Cafaro of Ventas, as an example of how good management can truly improve investment returns.

Debra Cafaro – Chairman and CEO, Ventas Inc.

Debra Cafaro has served as Ventas’ Chief Executive Officer since 1999 and as Chairman of the Board of Directors since 2003. At the time of assuming the CEO role, Ventas had a market capitalisation of just US$200m and was facing significant operating issues. Its largest tenant, Vencor Inc (98% of Ventas’ income) was working through bankruptcy as a result of changes to the re-imbursement of the skilled nursing industry. Vencor ultimately survived not least because of the lines of credit supplied by Ventas.

Vencor re-emerged as Kindred Healthcare (now one of Ventas’ largest operators), and Ventas’ market value has increased to US$22bn.

After studying Ms Cafaro’s history, we drew four lessons: the importance of track record and results, the fundamental understanding of risk, the courage to go against the grain, and the boldness to take a stand as an industry leader by making fact-based strategic decisions.

Lesson one – track record matters

Under Ms Cafaro’s leadership, the company not only turned itself around and became a market leading Healthcare REIT, it generated some impressive returns and track record along the way. From an operational perspective, between 2001 and 2016 Ventas had:

- annual Funds From Operations (FFO) per share growth of 11%;

- annual dividend per share growth of 10% per annum;

- maintained the annual dividend per share during and post-GFC; and

- received a credit upgrade during the GFC.

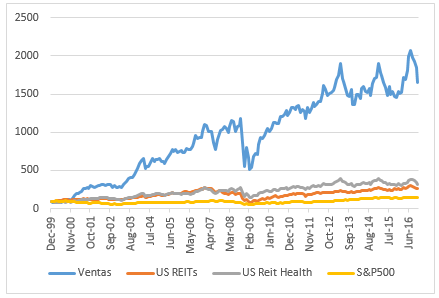

The share price performance was equally impressive since Ms Cafaro became CEO, reflecting the achievements above.

Source: Bloomberg, Quay Global Investors

Notably, most of the relative performance occurred up to and including the financial crisis.

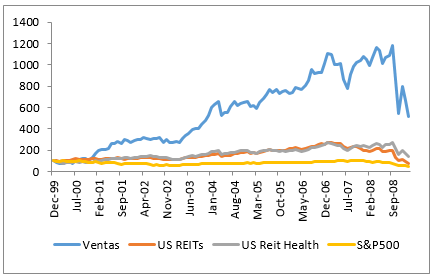

Source: Bloomberg, Quay Global Investors

After such impressive outperformance up to 2009, notwithstanding the outperformance of recapitalised distressed companies (‘junk rally’), Ventas consolidated its gains and continues to deliver attractive both total and relative returns in the post-GFC world.

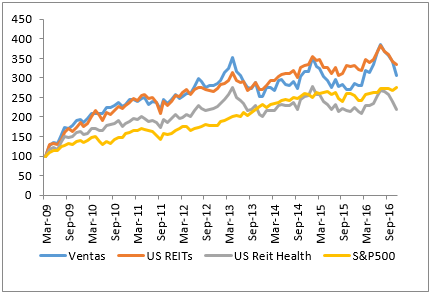

Source: Bloomberg, Quay Global Investors

Lesson two – good CEOs are the best risk managers

As we’ve quoted in prior Investment Perspectives, Warren Buffett once said that “risk comes in not knowing what you’re doing”. Good CEOs have an intuitive understanding of risk and manage it. Prior to the financial crisis, Ms Cafaro realised real estate pricing was becoming frothy. She convinced her management team that Ventas should limit new acquisitions.

By 2007, the company became “aggressively conservative”, raising equity and refinancing its debt while its stock price remained high. It also minimised acquisitions and pruned its portfolio, selling assets in order to pay down debt.

The parallels with Westfield Group (which also sold assets and raised substantial equity in 2007) are more than just a coincidence. It is a strategy hard to execute when peers are increasing leverage and growing earnings. Only companies with strong leadership and a good understanding of risk have the ability to undertake such a shift in the good times.

Lesson three – leadership matters when times are tough

Other events and strong economic conditions can mask management performance. CEOs can ‘ride the wave’ of good times and claim the credit. However, Ms Cafaro has demonstrated her ability to lead an organisation during very tough times. We discuss two examples below.

Prior to joining Ventas, Ms Cafaro was President of the listed REIT Ambassador Apartments. After taking the role, she discovered the company’s earnings projections were overstated and there was a risk of a potential default on credit agreements. After rectifying these issues within a year, the company stabilised and was sold to AIMCO for $680m.

Ten years later, the US was entering the largest financial crisis in 80 years. Having managed the company conservatively in the years prior (raising equity and selling assets), Ventas received a credit upgrade from S&P in the midst of the crisis.

Lesson four – good CEOs lead the industry

When pressed on the rationale behind a certain strategic decision, one of the more frustrating responses we receive is that they ‘listened to the market’. We prefer to back companies and CEOs that can see industry challenges and opportunities well before the market – even at the risk of near-term underperformance. When we invest in companies, we are backing management teams as industry leaders. If they’re reacting to the grumbles of equity holders, the risk is they begin to manage the company to meet short-term expectations – rather than generate long-term returns.

In 2007, Ventas became one of the first Health care REITs to invest in the operating performance of senior housing properties (prior to this, senior housing REIT investments were generally via a long-term lease to an operator). Recognising the value of capturing the long-term growth from demographics, Ventas moved early and has since built one of the premier senior housing operating portfolios in the US.

In 2015, recognising the emerging risks in Skilled Nursing Facilities, Ventas successfully spun-off its portfolio by mid-year. A year later, competitor HCP followed Ventas’ lead, while other peers are still selling down their exposure.

Summary

At Quay, our goal is to minimise risk by understanding our investees and the industry as best we can. However, we understand that despite our diligence, there are still many unknowns when investing. To account for this we seek to build diversified portfolios but just as importantly we look for investees that have, in our view, good leadership. We believe, Ventas is one such company.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular, this newsletter is not directed for investment purposes at US persons.