The macroeconomic landscape is mixed

2023 wrong-footed many macro-economic calls. Pundits overly devoted to the ‘inverted yield curve’ had predicted a US recession in 2023 with 100% certainty. What they got in return was accelerating GDP growth, declining inflation, and a strongly recovering global equity and property market.

So, what happened?

If there have been any economic lessons since the global pandemic (and indeed since the global financial crisis), it’s that strategists / markets tend to overstate the power of monetary policy while understating impact of fiscal policy.

We believe this is a useful starting point to frame the macroeconomic outlook for 2024.

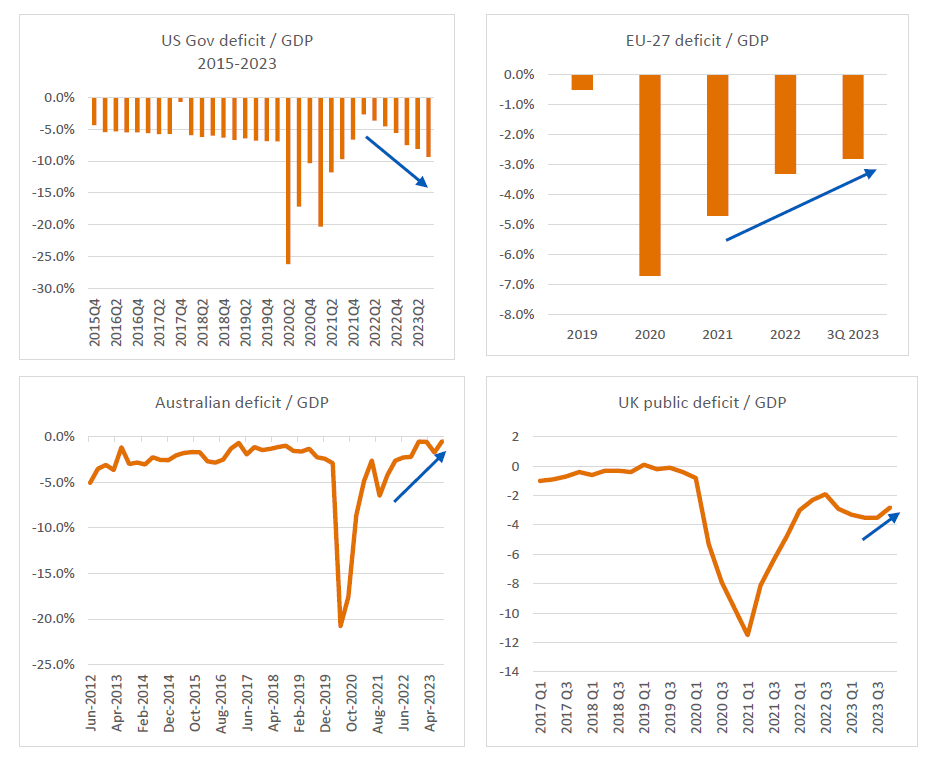

In summary, the US fiscal deficit continues to expand relative to GDP. This is largely due to a surge in net interest income on government debt driven by central bank policy. The deficit is adding income to the non-government sector, which continues to support growth and employment. In short, the near-term economic outlook for the US economy appears okay, albeit probably now moderating.

The story is different in other jurisdictions. Fiscal contraction in Australia, the EU and the UK point to further economic weakness.

Source: US Federal reserve Z.1 accounts, RBA, EuroStat, ONS UK, Quay Global

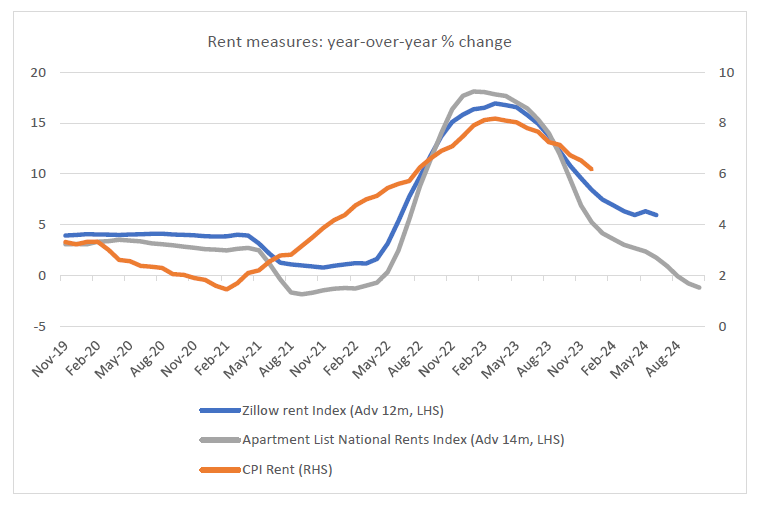

The good news is that non-US economic weakness will support interest rate cuts into 2024. Meanwhile, in the US, the well documented lag in CPI residential rents will feed into core and headline CPI, encouraging the US central bank to follow its Anglo peers and reduce rates into 2024. Worryingly, this is a very consensus market view, but it’s getting hard to ignore the data…

Source: BLS, Zillow, Apartment List

Global real estate asset class to rebound?

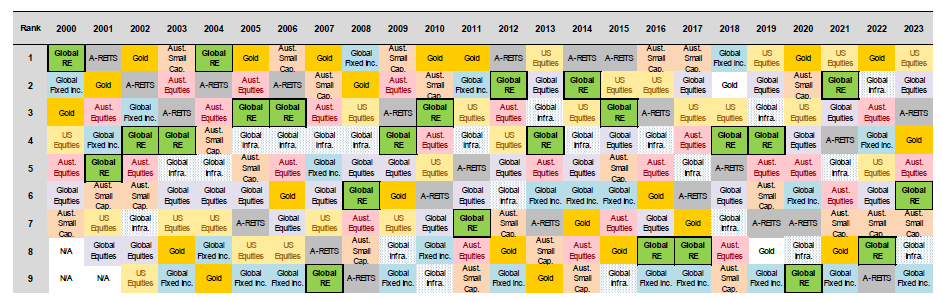

Notwithstanding the interest rate outlook, history suggests global real estate (unhedged) as an asset class tends to mean revert its performance relative to other assets classes over time. Below is the ranked performance of select asset classes since 2000. Global real estate has had a tough past two years, however, if history is a guide, the sector is due to bounce back (supported by the macro environment if our views are right).

As a general comment, it’s worth noting that so far this century global real estate:

- Ranks in the top three asset classes nine times versus global equities (five times), and Australian equities (eight times)

- Ranks in the top four asset classes 15 times versus global equities (six times) and Australian equities (10 times).

Source: Bloomberg, Quay Global Investors

Global real estate - asset class themes and thoughts

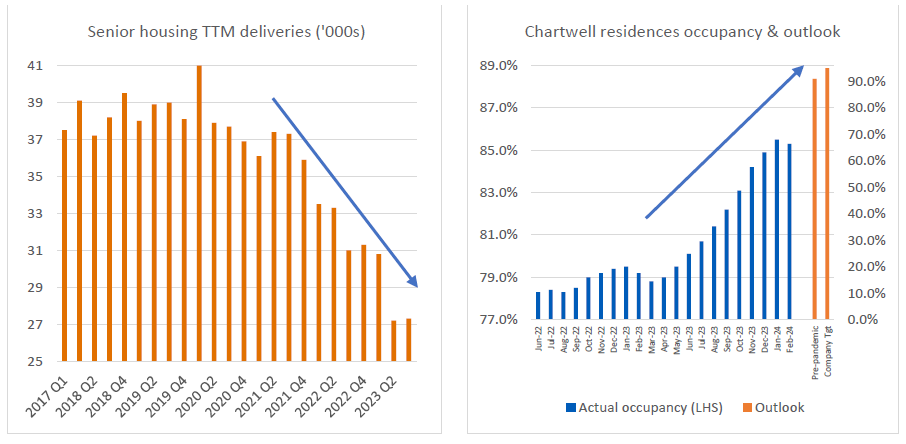

Senior housing: the long demand cycle is only just beginning

Next year is 2025 and will mark the 80-year anniversary of the end of the second world war. Why is that important? Because it also signals that next year, the first of the Baby Boomers will turn 80 – an age where many turn to some type of assisted living.

That’s good news for the senior housing industry, which is still recovering from the pandemic (both operationally and share price-wise). Assisted living via senior housing is a needs-based industry and relatively immune to economic conditions. Despite the expected surge in demand, net new supply is at a cyclical low (due to high construction costs). The result is accelerating occupancies gains, enhanced pricing power and ultimately robust earnings growth as seen by leading senior housing owners like Chartwell Residences.

Source: Welltower, Chartwell, Quay Global Investors

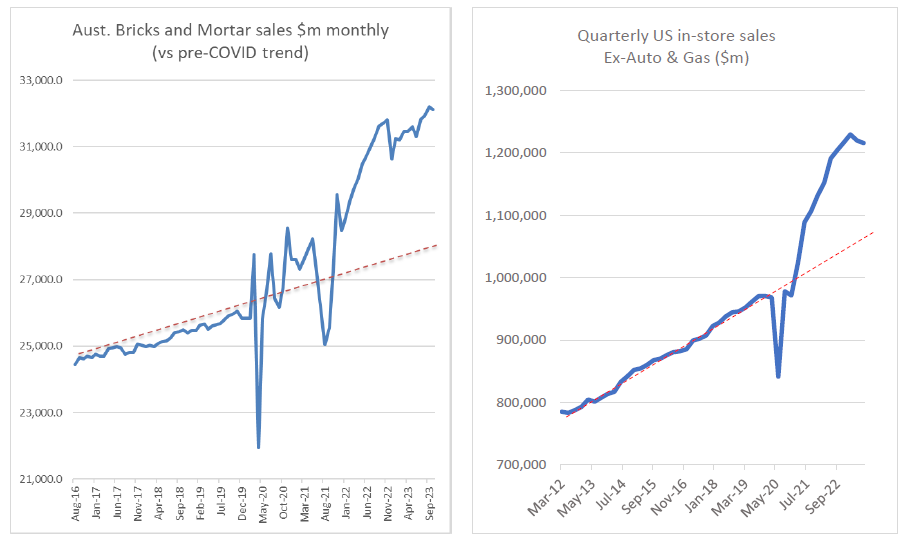

Brick and mortar retail – is there more operational upside?

The ageing demographic story is well known, and therefore may represent crowded trades – so an eye on valuation is paramount.

Maybe less obvious is the phoenix-like rise of brick and mortar retail in the post-pandemic world.

One of the better performing REITs in 2023 was US mall owner, Simon Property Group, which delivered 26% total return versus the global REIT index of 9%. Despite the performance, there could be more for the retail story.

As we noted in our 2023 article, Why best-in-class mall rents are recession resilient, the relatively fixed nature of small shop (specialty) leases means there is a lag between the operating performance of a mall, and its current financial performance.

The recovery in store retail sales since COVID remains well above the prior pandemic trend. Retailers continue to make hay while the sun shines, as their in-place rents still largely reflect a pre-COVID world. Expect good financial results from the best malls in 2024 as landlords continue to mark rents back to economic reality.

Source: ABS, BLS, Quay Global

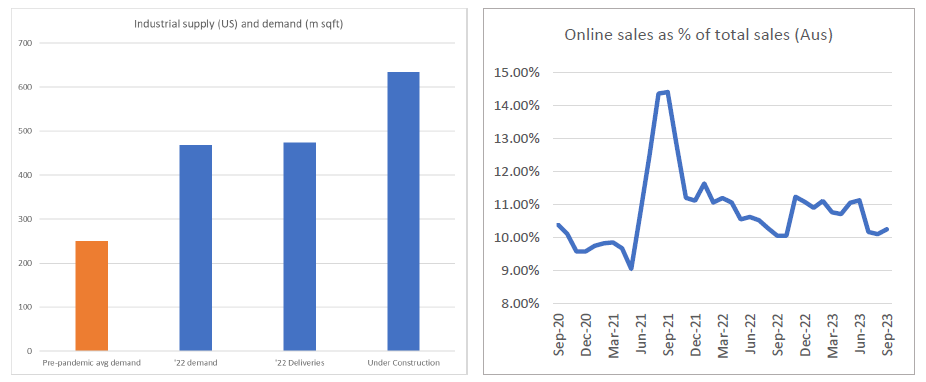

Industrial - a time to be cautious

It’s hard to imagine a sector that has benefited from more successive tailwinds. The secular growth in e-commerce, COVID and lockdowns, China’s slow re-opening, the move to ‘onshoring’, and the shift to ‘just in case’ inventory management. It seems every major economic shift over the past decade has been to the advantage of industrial tenant demand.

As with most forms of real estate, investment success is a double-edged sword. Along with investment demand comes the incentive to build new supply. Landlords currently believe this pipeline (see below) is manageable. Time will tell.

Meanwhile, the sector ecommerce story is slowing while valuations continue to reflect investor enthusiasm. We think 2024 is the year to be cautious in this subsector.

Source: JLL, Quay Global Investors

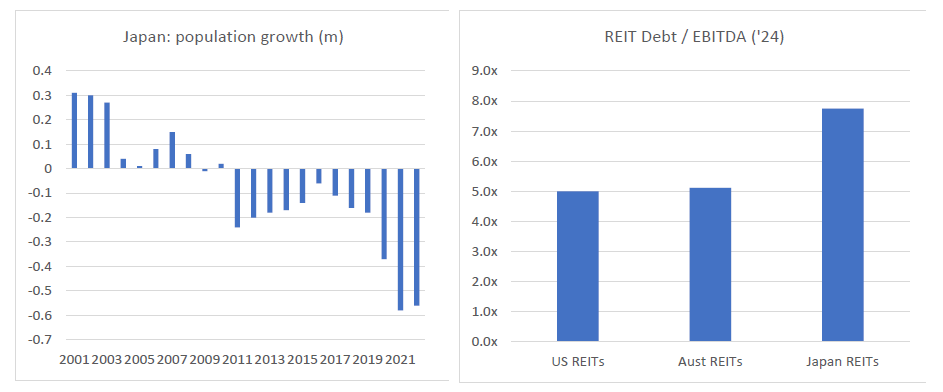

Japan’s demographics may attract more headlines

Our December 2023 article, 12 surprising charts for your Christmas stocking, we highlighted the steady decline in Japan’s population since 2010. The 2023 number should come out later this year, however the trend is clear. Even without new construction, falling population will mean real estate vacancy rates will begin to rise, rents will begin to fall, and asset values will decline.

From a real estate perspective, that’s bad news. However, like most financial systems, local banks and investors find most of their collateral and security via real estate. The demographic headwinds may begin to pose a risk to entities that hold loans and mortgages backed by real estate.

As the fourth largest economy in the world, we expect this trend will begin to attract wider attention in 2024.

Source: World data, Quay Global Investors, UBS

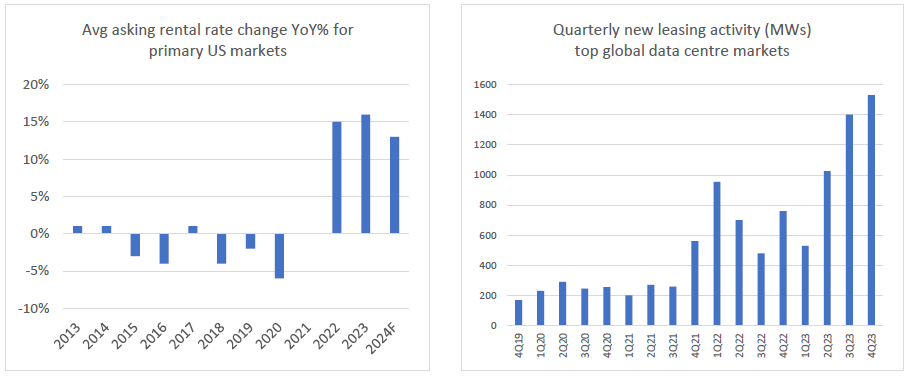

Data centres

Data centre fundamentals are likely to remain strong in 2024. Demand will continue to outpace supply, placing pricing power in favour of lessors. In 2023 we saw record new leases signed and accelerating lease spreads. Vacancies are also at record lows, meaning the only option is to build new, and we expect more development projects to be announced in 2024. However, these projects are either pre-committed and/or have five year plus delivery timelines, as sourcing enough power, land and equipment remains a challenge. Our team attended a US data centre tour in November 2023, where we learnt that in markets such as Los Angeles, there is up to a seven-year wait to secure power for developments.

Despite the structural tailwinds, we do not expect outsized earnings growth for the sector in 2024. The long duration (10-15 year) nature of hyperscale leases means a significant portion of current rental rolls were signed back when leasing environments were less favourable. Annual rents bumps were closer to 2% than the 5%+ it is now for new deals. Landlords are trying to speed up this process by divesting ‘low growth’ data centres and reinvesting capital into new developments. Nevertheless, it will take time to play out, but the trend is positive.